Whether you are a new or established small business owner, you might need extra funding at some point. You might be renovating, adding employees to payroll, or upgrading equipment. A business loan can help you pay for large expenses and grow your company. You need to know how to get a small business loan and which financing option is best for you. Take a look at the small business loan tips below.

How to get a loan to start a business

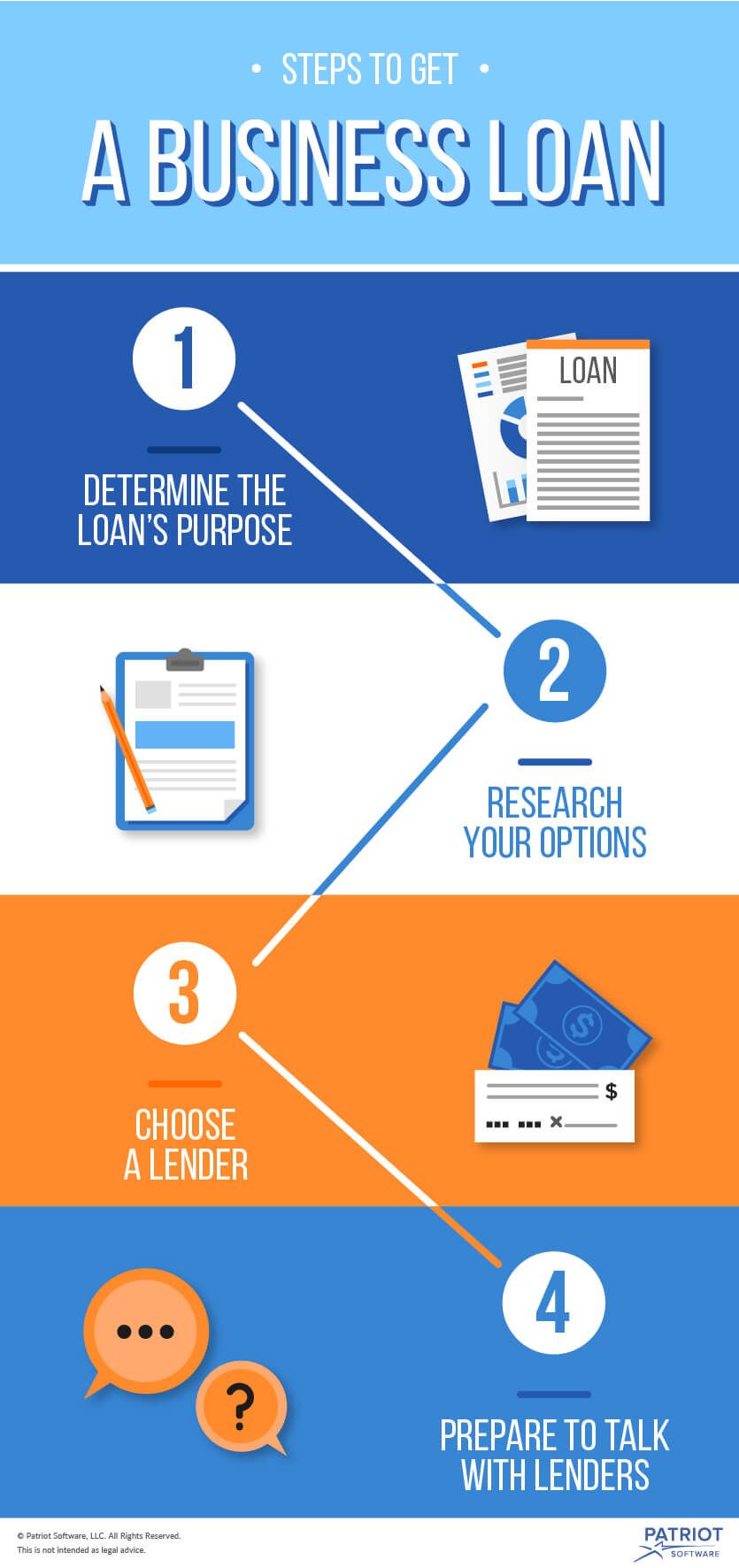

You can pursue either debt funds vs. equity funds for your business financing. Are you considering financing your startup or small business with a loan? Follow these four steps to getting a small business loan.

1. Determine the loan’s purpose

The first thing you need to do when getting a loan for a business is determine how you will use the money. Evaluate your need for the loan and pinpoint what you will put the funds towards.

There are many ways you can use a business loan. If you’re a new entrepreneur, you might be getting a loan to start a small business. Or, you might be an established business owner wanting to grow your company. You could also use a loan to catch up with daily operating expenses. You might also want to create a cash reserve as a safety net for unexpected costs with a business loan.

Once you have a grasp on your intentions for the funds, develop a detailed plan for its use. Lenders want to see that the money will go towards a specific purpose. To convince lenders you will meet financial benchmarks, create a compelling story about your business and be able to explain your plan confidently and clearly.

2. Research your loan options

There are many small business loans options available. Your needs, equity, and credit history are all factors in determining which loan is right for you.

SBA loans

A good place to start when searching for a loan is the Small Business Administration (SBA). SBA loans are available to both operating companies and startups.

The SBA does not directly lend money. Instead, the SBA backs a bank loan with a partial guarantee. If you can’t make payments on the loan, the SBA takes on some responsibility. The guarantee reduces the lender’s risk, so you have a better chance of securing the loan.

SBA 7(a) loan

The most common SBA loan program is the 7(a) loan. You can use the 7(a) loan for a variety of purposes, including working capital, equipment, real estate, renovation, and refinancing.

To secure a 7(a) loan, you must meet several SBA loan requirements. You need to operate for profit, be a small business, and have reasonable owner’s equity, among other factors. Visit the SBA website for a full list of eligibility requirements.

The 7(a) loan lets you borrow up to $5 million. The SBA can guarantee up to 85% of the loan for loans up to $150,000. For loans over $150,000, the SBA can guarantee up to 75% of the loan amount.

SBA microloan

For a smaller SBA loan option, you could apply for a microloan. Microloans are a good route for getting a loan to start a business.

The microloan program lends up to $50,000. The average amount of a microloan is $13,000. You can use a microloan for working capital, inventory, equipment, and furniture.

You can repay microloans for up to six years. Your interest rate will vary, but rates are usually between 8% and 13%. If approved, you need to go to training sessions about how to be cost effective with your loan.

Other financing opportunities

As a small business owner, you have small business funding options other than an SBA loan. Depending on your needs, you will want to consider different kinds of loans. The following are common small business purposes for borrowing and the loans you should pursue.

Getting a loan to open a business

It’s very difficult to secure a business loan during your first year of operating. You do not have proof that your business will make a profit, so the risk of lending to you is high. There are some startup business loans available to new business owners.

As a startup owner, you could pursue a nonprofit microlender. Nonprofit microlenders provide small loans to help startups, small businesses, and underprivileged and underrepresented communities succeed.

Even if you have a poor credit score, you might be able to get a nonprofit microloan. A nonprofit microloan is a small business loan that may be available faster than a traditional bank loan.

If you are not approved for a loan, consider borrowing from friends and family, opening a business credit card, taking out a personal loan for business, or crowdfunding.

Getting a loan to buy equipment

Your business might need to invest in new equipment. Funding these purchases can be done through an equipment loan.

Equipment loans can be used for vehicles, machines, and other equipment necessary to run your business. The loans give you quick access to money and cover up to 100% of the equipment’s value. Equipment loans have fixed interest rates, meaning the percentage of interest does not change. The payment plan lasts the life of the equipment.

Managing cash flow and daily operations

Dealing with the inflows and outflows of cash can be tough. Sometimes, you need help covering costs when cash is low. To cover day-to-day operations, you have several business loan options.

- Business lines of credit let you borrow only the money you need. You are approved for a borrowing limit, similar to a credit card. You can use the money as you need it.

- Working capital loans cover everyday expenses and have low financing rates. Use these loans to get through seasonal changes in business and months when your small business cash flow is lower than usual.

- Invoice factoring provides you with cash up front and is used for unpaid invoices. Business invoice factoring covers short-term needs when customers are slow to pay.

- Online lenders use formulas based on traditional and nontraditional credit values to decide your loan terms. Usually, online lenders provide funds faster than traditional banks and credit unions.

Growing an existing business

You can expand your company with a business term loan from the bank. Term loans have fixed interest rates. You make monthly payments over a period of years. With a business term loan, you receive a lump sum of cash upfront. Use these loans to invest in your existing business.

3. Choose a lender

Business loans come from different lenders. As you search for a lender, look at annual percentage rates and the total borrowing cost of the loan. The total borrowing cost is the amount of the loan plus interest.

For the smallest total borrowing cost, try to choose a loan with the lowest annual percentage rate. Also, carefully review the loan terms and be sure you will be able to make regular payments.

You can get a business loan from a bank, nonprofit lender, or online lender. After choosing a type of loan, compare options between several lenders.

- Bank loans work for businesses with collateral, good credit, and no need for immediate funds. As a small business, you might have trouble securing a bank loan. The lower your annual sales and cash reserves, the riskier you are to the bank. Usually, it takes a longer amount of time to get a bank loan than other lenders.

- Nonprofit lenders, or microlenders, offer short-term loans. The interest rate is usually higher than a bank loan. Try to secure a loan from a microlender if you are not approved by the bank.

- Online lenders help small businesses that don’t have collateral and need funds fast. Loan amounts and interest rates vary widely, so shop around before choosing a lender. Though interest rates are often higher than bank rates, you can secure a loan with an online lender faster. It may also be easier to secure a business loan from an online lender than a bank.

Forming a relationship with your lender often makes securing financing easier. You can build trust with lenders by opening accounts with the lender you want to borrow from. To maintain a good history between you and the lender, avoid late payments and overdrafts.

4. Prepare to talk with lenders

When you apply for a business loan, don’t approach lenders empty handed. You need to convince them that you need the loan and you will be able to repay the money.

Lenders will request financial information about you and your business. You will need to report your annual revenue to prove your business makes money. You will also need your average bank account balances to show how well you manage money.

Report both your personal and business credit histories to the lenders. And, give lenders more information about your finances by providing past tax returns.

Create a formal, comprehensive small business plan to give lenders an overview of your business’s financial health. The plan should include financial statements that report annual sales and profitability. Also, include cash flow projections that predict future influxes in funds.

Provide information about how long you have been operating your business to the lenders. You will also need a personal guarantee to secure the loan. A personal guarantee makes you legally responsible for loan repayment. Your personal property could be at risk if business income doesn’t cover the loan.

Do you need a simple way to keep track of your small business funds? Patriot’s online accounting software is easy to use and made for the nonaccountant. We offer free, U.S.-based support. Try it for free today.

This article has been updated from its original publication date (6/21/2016).