No matter the size of your company, there is always a need for capital in order to operate and grow. For small business owners, one funding option is a personal loan. These loans focus on your financial history, not your business’s. Find out if a personal loan for business is right for you.

Questions to ask before using a personal loan for business

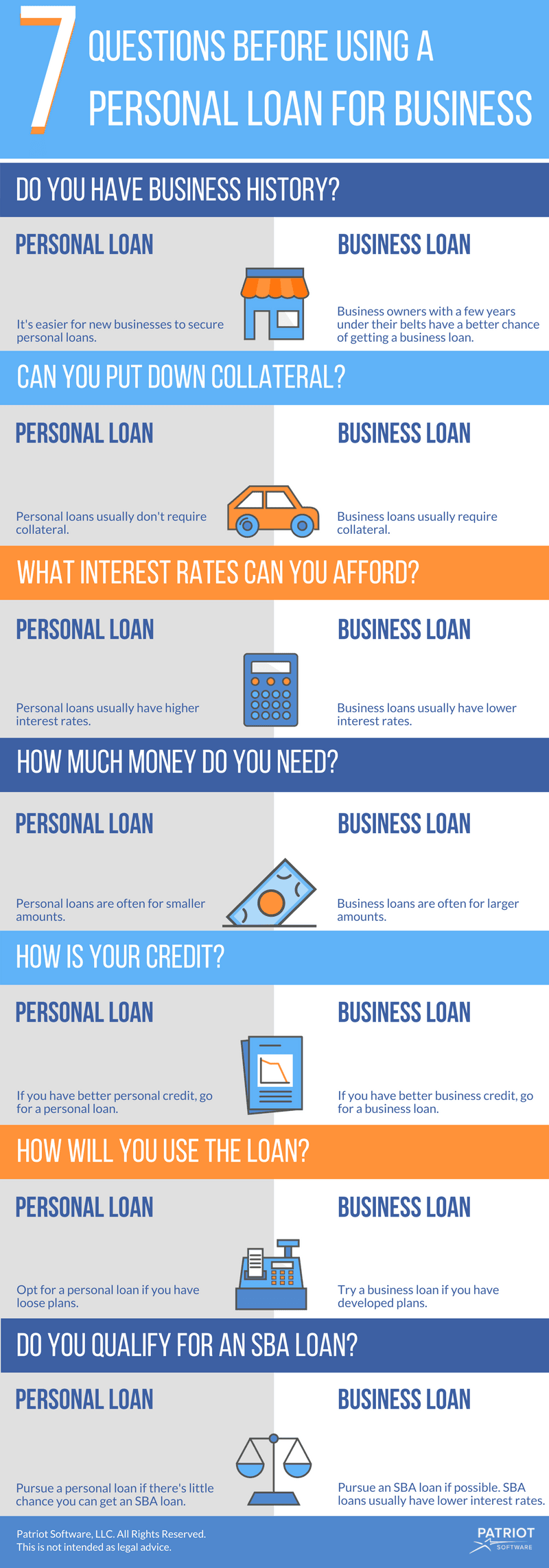

Some business owners choose to finance their companies with personal loans, while others use business loans. Take a look at these seven questions to ask when comparing loans for startups.

1. Do you have a business history?

Depending on how long you’ve been in business, a personal business loan might be a good funding solution. Banks often review how much experience you have operating a company before you qualify. Lenders want to know that you can pay back the loan with revenue generated by your business.

You are opening a new business: If you haven’t opened the company yet, consider a personal loan for business. You do not need to have business experience to secure small business personal loans. Lenders do not ask for business information or records.

You own an established business: Veteran owners are more likely to be granted a business loan than new entrepreneurs. To get this kind of loan, you need to show a small business plan, cash projections, and business financial statements. The documents prove your business generates enough income to pay the loan.

2. Are you willing to put down collateral?

Collateral is a piece of property you offer a lender as security for the loan. If you fail to pay the loan according to the terms, you might need to give your collateral to the bank. Since lenders use the seized items to cover loan payments, it reduces their level of risk.

You don’t have many assets: Personal loans are usually unsecured, meaning you do not need collateral. If you don’t have many items to offer as security, there’s no need to worry.

You have a lot of assets: Business loans are often secured loans that require collateral. If you want a business loan, you will need to offer lenders some security. Learning how to get a business loan might be a good choice for a company with a lot of assets. Usually, the trade-off for having to offer business collateral is lower interest rates.

3. What interest rates can you afford?

Because of interest, you end up paying more than the loan amount granted. How much more depends on the loan. The higher the interest rate, the more the total loan amount will be. Interest rates vary when it comes to personal and business loans.

You can handle higher interest rates: Personal loans to start a business tend to have higher interest rates than small business loans. This is because personal loans are unsecured and have less strict terms for use. Consider a personal loan for business if the benefits outweigh the cost of interest.

You need low interest rates: Often, business loans for startups have lower interest rates. If you require small lending fees, a business loan might be your best option. The total amount you pay could be less than with a personal loan.

4. How much money do you need?

A major factor in choosing a loan is the amount of money you need. You can get a loan for countless reasons, from buying equipment to leveling cash flow. Different types of loans offer various borrowing limits.

You need a small amount: Personal loans are usually granted in smaller amounts than business loans. Consider a personal loan if you think you can pay the debt fast. Paying a small amount off quickly could prevent you from having issues with debt.

You need a large amount: To get a large amount of capital, go for a business loan. Small business loans are usually offered in larger amounts because they are secured. If the amount of a personal loan is not enough, you might need to pursue small business funding options.

5. How is your credit?

Any time you attempt to secure a loan, lenders look at your credit score and financial history. Look at your personal and company finances. Each type of loan focuses more on either personal or business money.

You have better personal credit: Personal loans require good personal credit and finances. Your business credit score has nothing to do with getting a personal loan. If your business has poor or unestablished credit, consider a personal loan.

You have better business credit: Lenders dig deep into your company’s financial history for business loans. If your company has a lot of assets, steady cash flow, and a good business credit score, go for a business loan.

6. How will you use the loan?

Depending on your plans for the borrowed funds, you will need a personal or business loan. Hone in on how you will use the money before pursuing a loan.

You have loose plans for the money: Personal loans can be used for just about anything. Since the loan doesn’t directly involve your business, you do not need to present an elaborate plan to lenders. The terms for how you can use the money are flexible.

You have a developed plan: A business loan usually has a specific purpose, such as to fix a problem or expand a business. Because there are a lot of moving parts to a business, lenders set strict terms for how you can use the money.

7. Do you qualify for an SBA loan?

The Small Business Administration offers several loan programs for small business owners. The loans are bank loans guaranteed by the SBA. The guarantee reduces the bank’s risk level, making it easier for small businesses to get approved.

It’s not likely you will be approved for an SBA loan: If you don’t believe your business will qualify, or you’ve already been denied, consider a personal loan. The personal loan process is faster than securing an SBA loan.

You will likely get approved: Though it takes longer to get approved, SBA loans usually have lower interest rates and higher borrowing limits. If you’re not in need of quick cash, filling out an SBA loan application could be worth the wait.

Need a simple way to track your business funds? Patriot’s online accounting software is easy-to-use and made for the non-accountant. We offer free, U.S.-based support. Try it for free today.