Are you self-employed? If so, you better keep reading. Self-employed individuals must pay a unique payroll tax called self-employment tax. What is self-employment tax?

In this article, you’ll find out everything you need to know about self-employment tax. Learn how much the tax is, how to calculate your tax liability, and more.

What is self-employment tax?

Self-employment tax is a type of payroll tax that self-employed individuals must pay to cover their Social Security and Medicare tax liabilities.

Employers withhold Social Security and Medicare taxes from employee wages in the form of FICA tax. There is also an employer portion of FICA tax that employers are responsible for paying. Employees pay 7.65% for the employee portion of FICA tax, and employers pay a matching 7.65% for the employer portion.

Unlike employees, nobody withholds and contributes FICA tax (Social Security and Medicare taxes) for self-employed individuals. Self-employed individuals must pay their Social Security and Medicare tax liability on their own.

It’s not uncommon for business owners to wonder if they are responsible for paying self-employment tax. Anyone who is self-employed must pay the tax.

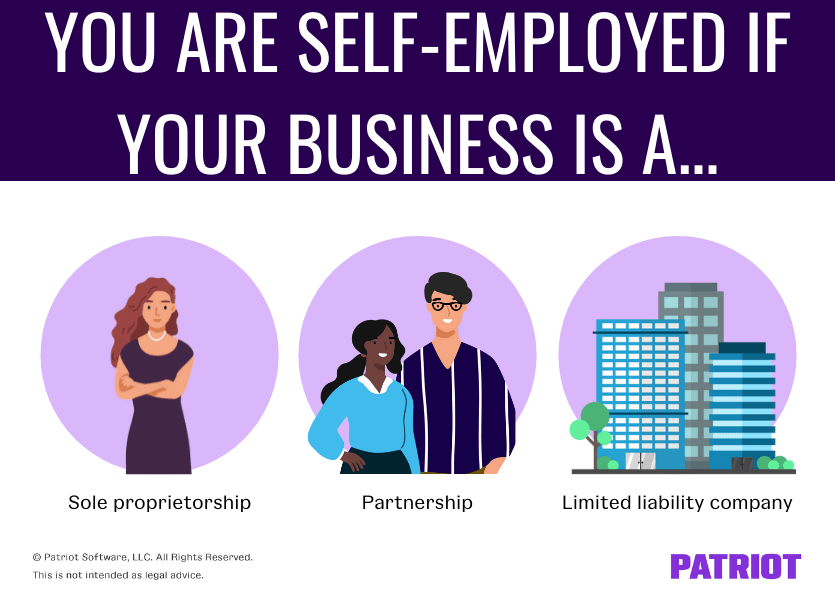

So, what does self-employed mean?

You are considered self-employed if you own an unincorporated business. This includes businesses structured as sole proprietorships, partnerships, and limited liability companies (LLCs).

If you are self-employed, you must pay self-employment tax if your net earnings from self-employment are $400 or more per year.

There are no age limits to paying self-employment tax. You must pay the tax regardless of your age, even if you are already receiving Social Security or Medicare benefits.

Self-employment tax only pays for Social Security and Medicare taxes. It does not cover federal, state, or local income taxes. You still need to pay income taxes on your own.

How much is self-employment tax?

The self-employment tax rate is 15.3% of your annual earnings.

Think of the tax tax as the equivalent of paying both portions of FICA tax (7.65% employee portion + 7.65% employer portion = 15.3% total).

Of the 7.65% FICA tax rate, 6.2% goes toward Social Security tax and 1.45% goes toward Medicare tax. This applies to both the employee and employer portions.

The 15.3% self-employment tax rate is also broken down into two parts: Social Security and Medicare taxes. Of the 15.3% rate, 12.4% goes toward Social Security tax and 2.9% goes toward Medicare tax.

Knowing the percentages that go toward Social Security and Medicare taxes is essential for correct calculations.

Why? There is a Social Security wage base as well as an additional Medicare tax.

Social Security wage base

You must pay the 12.4% Social Security portion of self-employment tax until you earn above the Social Security wage base. This wage base is subject to change annually.

For 2022, the Social Security wage base is $147,000.

Once you earn above the wage base, stop contributing the 12.4% portion.

Additional Medicare tax

Unlike Social Security tax, there is no Medicare wage base. Instead, there is an additional Medicare tax that applies after you earn a certain amount.

The additional Medicare tax rate is 0.9% after you earn above the additional Medicare tax threshold. The threshold depends on your filing status:

- Single: $200,000

- Married Filing Jointly: $250,000

- Married Filing Separately: $125,000

- Head of Household With Qualifying Person: $200,000

- Qualifying Widow(er) With Dependent Child: $200,000

When you earn more than $200,000 (single, head of household, qualifying widow), $250,000 (married filing jointly), or $125,000 (married filing separately), your new Medicare tax rate becomes 3.8% (2.9% + 0.9%).

How to calculate self-employment tax

Calculating self-employment tax is relatively straightforward. Multiply your wages by 15.3% to find your self-employment tax liability.

If your earnings are above the Social Security wage base, stop multiplying your earnings by 15.3%. Instead, multiply your earnings above the wage base by 2.9%.

If your earnings go beyond $200,000 (single), you must start multiplying your earnings by the additional Medicare tax rate. Multiply your earnings above $200,000 (single) by 3.8%.

Confused, or just a little uncertain? Let’s see it in action with the example below.

Self-employment tax calculation example

Let’s say you earn $205,000 in self-employment wages in 2022. You are a single-filer. To calculate your self-employment tax liability, remember the following information:

- 15.3% tax rate on first $147,000 of earnings

- 2.9% tax rate on earnings after $147,000

- 3.8% tax rate on earnings after $200,000

First, let’s calculate your tax rate up to the Social Security wage base. To do this, multiply $147,000 by 15.3%:

$147,000 X 0.153 = $22,491

Next, multiply the difference between $200,000 and $147,000 (= $53,000) by 2.9%. This represents your earnings that are only subject to Medicare tax:

$53,000 X 0.029 = $1,537

Now, multiply the difference between $205,000 and $200,000 (= $5,000) by 3.8%. This represents your earnings that are subject to the regular Medicare tax rate and additional Medicare tax rate:

$5,000 X 0.038 = $190

Lastly, add up your wages subject to both Social Security and Medicare, your wages subject to only Medicare, and your wages subject to both Medicare and additional Medicare:

$22,491 + $1,537 + $190 = $24,218

Your tax liability for self-employment for the year would be $24,218.

How to pay self-employment tax

You must have a Social Security number (SSN) or an Individual Taxpayer Identification Number (ITIN) to pay the tax.

Most self-employed individuals pay the tax by filing estimated taxes quarterly. Estimated taxes include liabilities like self-employment and income taxes.

You have a few options for paying estimated tax. You can pay online, by phone, or by check or money order using the estimated tax payment voucher.

Is there a specific self-employment tax form you can use? Use Form 1040-ES, Estimated Tax for Individuals, to help you determine your estimated tax liability, submit payments by check or money order, and view more payment information.

Tax due dates

You can either pay your total estimated tax bill April 15 or split it into four equal amounts. If you choose to make quarterly estimated tax payments, your due dates are:

- 1st payment: April 15

- 2nd payment: June 17

- 3rd payment: September 16

- 4th payment: January 15

Tax deduction

Your tax liability for self-employment can get pricey. Luckily, you can deduct the “employer” portion of the tax, which is 7.65%.

The self-employment tax deduction only affects your adjusted gross income and income taxes. You must still pay the whole self-employment tax rate of 15.3%.

Payroll taxes can be complicated. That’s why Patriot offers Full Service payroll services. We make payroll easy by filing and remitting payroll taxes on your behalf. Start your free trial today!

This article has been updated from its original publication date of August 13, 2014.

This is not intended as legal advice; for more information, please click here.