During the process of building your business, you might need small business loans at some point. Business loans can help you through difficult times or help fund expansion.

Getting a small business loan can be tough. It’s not as simple as applying for a small business loan and then receiving a bunch of money. It’s imperative that you don’t make any mistakes while getting your small business loan.

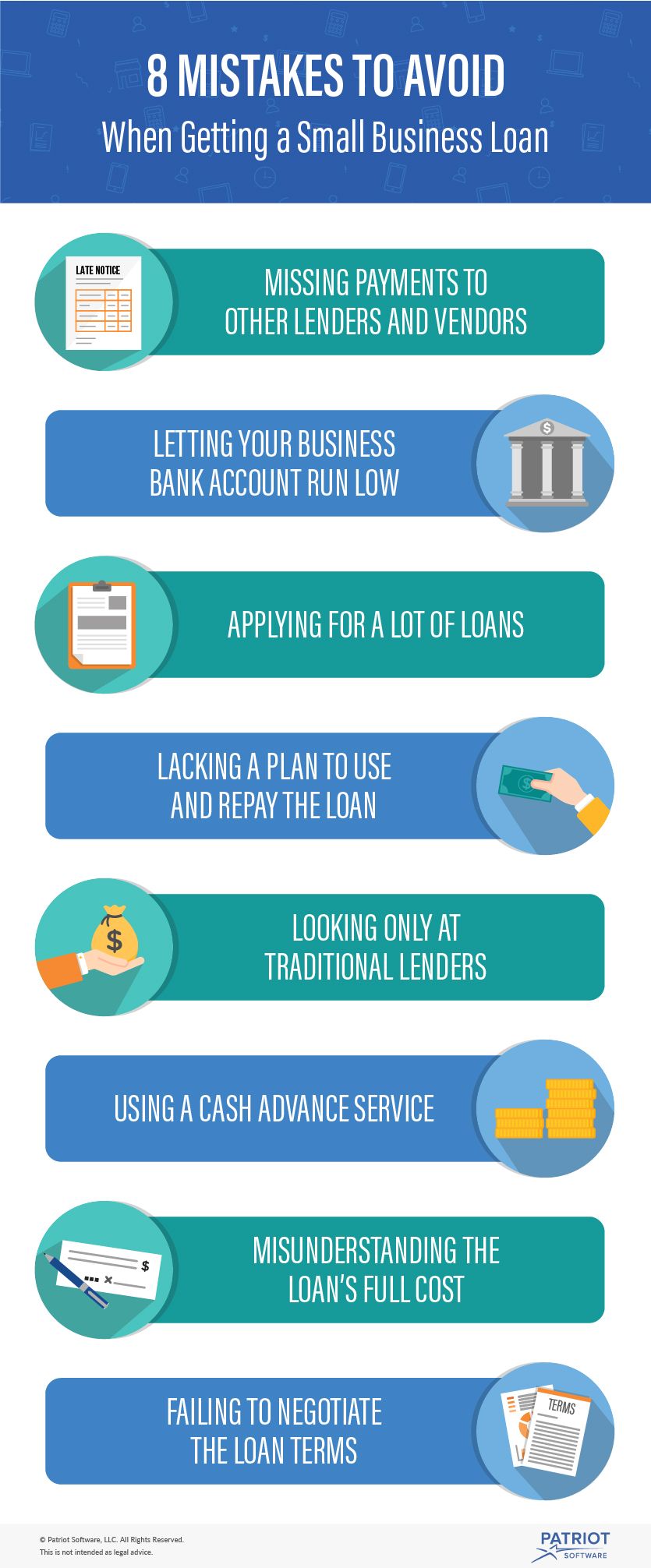

Mistakes when getting small business loans

You have the potential to make many mistakes when getting a small business loan. Your mistakes might prevent you from getting a loan. Or, you might not be able to pay back the loan later. Use the business loan tips below to avoid making mistakes when you try to get a loan.

Missing payments

If you miss payments on other bills, that’s a red flag for lenders. Lenders will see your missed payments and think you will fail to pay toward your business loan, too.

Regularly pay off your business credit cards, vendor accounts, and other accounts that report to personal or business credit reporting agencies. Make sure your payments are on time. You want to build a good track record for yourself.

Letting your account run low

You might need a loan because your business’s funds are running low. But, you shouldn’t let your bank account run too dry.

If your business bank account has barely any money in it, lenders might think you won’t have enough to pay back the loan. And if a lot of money leaves your account, but not much goes back in, lenders might think you have negative cash flow.

Applying for a lot of loans

To improve your chances of being accepted for a loan, you might apply for a lot of loans. If you apply for a lot, you’re bound to get approved for one of them, right?

Applying for a lot of loans can actually hurt your chances of getting any of them. Lenders will check your small business credit score. Each time your credit score is pulled, it takes a small hit. As your credit score gets smaller, lenders will think of you as an unappealing loan candidate.

Apply for loans strategically. Fill out a small business loan application only for the loans you actually want and qualify for.

Lacking a plan

Not all lenders will require a formal business plan. However, you should still have a plan.

You should have an idea of what your business’s future looks like. Figure out what your projected expenses and growth look like.

One of the biggest benefits of a business plan is the confidence that it can instill in lenders. Your plan shows that you aren’t going to take their money, never to be seen again. Having a plan demonstrates that you know how you’ll use the loan and pay it back.

Looking solely at traditional lenders

When you think about getting a loan, your first thought might be to go to a bank. But, bank loans aren’t a good fit for every business. For example, a bank loan will be more difficult to obtain if you or your business has a low credit score.

Check out alternative small business lenders. Alternative lenders are any lenders outside of a bank. Research online lenders, lines of credit, invoice factoring for small business, and other small business funding options.

Using a cash advance

You can get cash advance business loans. These loans are similar to personal payday loans.

You have a great potential of drowning your business in debt with a cash advance loan. These loans often have high interest rates and short payoff times. You will potentially accumulate debt faster than you can pay it off. Also, business cash advance loans often take a portion of your future sales, putting your business on financially unstable ground.

You might be able to use a cash advance loan and be fine. But, be cautious and know the full terms and risks in advance.

Misunderstanding the full cost

Comparing two loans can be like comparing apples and oranges. Not all lenders describe their loan terms in the same way, making it difficult for you know the right option for your business.

Find out the annual percentage rate (APR) for each loan you are considering. The APR is your annual cost, including any fees. It reflects the total cost of the loan, not just the interest rate.

You should know the total length of the loan. A shorter or a longer loan might be a better fit, depending on your business’s needs and ability to pay back the loan.

You should also find out if there are any fees for paying off the loan early, called prepayment penalties. Not all small business loans have prepayment penalties. Make sure you read and understand the full terms of your business loan before you agree to it.

Failing to negotiate

Business loans aren’t as set in stone as you think. You might be able to negotiate better terms that will benefit your business, especially if you get your loan through a bank. For example, you might be able to reduce the interest rate or remove fees.

Do you need a simple way to track your business’s finances? Patriot’s online accounting software is made for the nonaccountant. You can easily monitor your cash flow and business loans. Try the software for free.