Businesses could apply for a Paycheck Protection Program loan through May 31, 2021. As of June 1, 2021, the SBA is no longer accepting PPP loan applications.

This article applies to PPP loans taken out in 2020. The Consolidated Appropriations Act (signed into law on December 27, 2020) reopened the Paycheck Protection Program and made changes to it.

Ah, this is the moment most Paycheck Protection Program (PPP) loan borrowers have been waiting for. The Paycheck Protection Program Flexibility Act was signed into law, bringing significant changes to the PPP.

Are you a PPP loan borrower who wants to know what the PPP Flexibility Act will do for you? Read on to find out.

What is the Paycheck Protection Program Flexibility Act?

The Paycheck Protection Program Flexibility Act is coronavirus-related legislation that amends the CARES Act to make PPP loan forgiveness easier on small business owners. It was proposed in the House of Representatives and passed by the House on May 28, 2020. The act was then passed by the Senate on June 3, 2020 and signed into law by the president on June 5, 2020.

The PPP Flexibility Act is the second piece of legislation focused on expanding the PPP, after the PPP and Health Care Enhancement Act.

The PPP and Health Care Enhancement Act, which was signed into law on April 24, 2020, added an additional $310 billion in funding to the program.

Unlike the PPP Health Care Enhancement Act, the PPP Flexibility Act does not add more funding to the program. However, it extends a number of rules to benefit small business owners and increase loan forgiveness potential.

What the PPP Flexibility Act changes

The PPP Flexibility Act is a relatively short bill. There are six major changes the PPP Flexibility Act makes to the PPP:

- Eligible expenses flexibility

- Covered period extension

- FTE reduction exemption

- Loan repayment deferral period extension

- Loan term extension

- Payroll tax deferral expansion

Check out what each rule was under the CARES Act and what it now is under the PPP Flexibility Act.

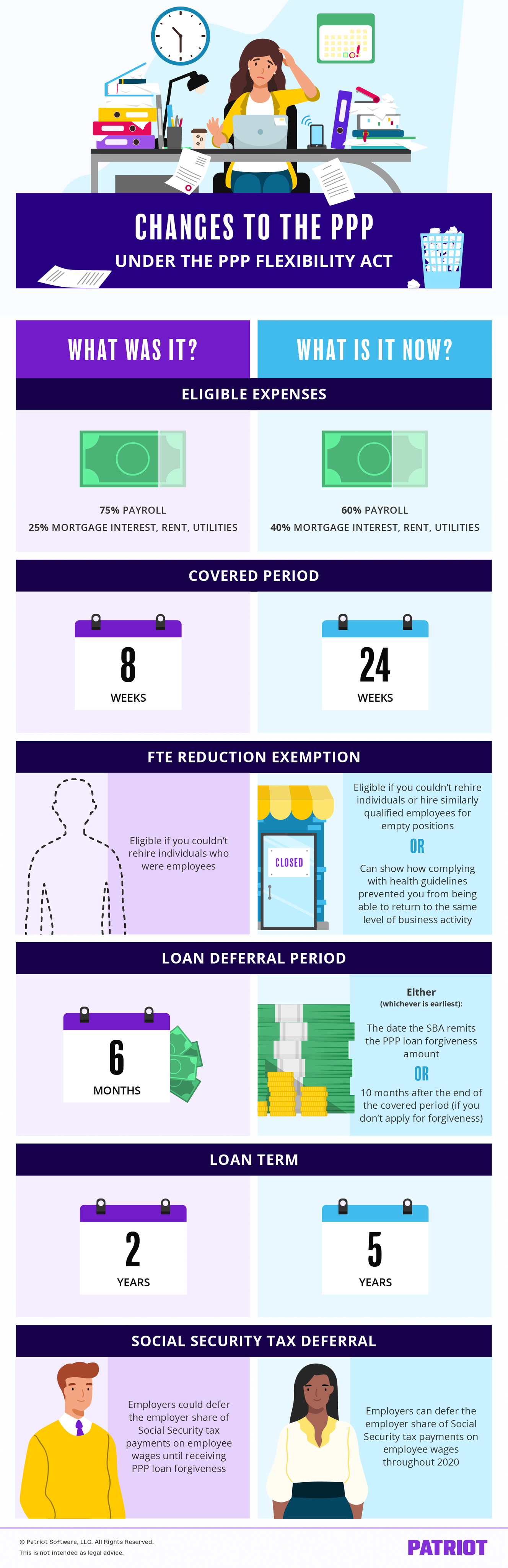

1. Eligible expenses (60% / 40%)

As you well know, you must use the PPP loan to cover eligible expenses if you want it forgiven. And, the SBA and Treasury specify how much you should use for what expenses.

Originally, the SBA and Treasury required you to use 75% for payroll expenses and 25% for mortgage interest, rent, and utilities.

Thanks to the Paycheck Protection Program Flexibility Act, you can now use 60% on payroll expenses and 40% for mortgage interest, rent, and utilities. This gives you more wiggle room to spend on non-payroll costs.

2. Covered period

Under the CARES Act, you had eight weeks to use your PPP loan on eligible expenses. This eight-week covered period began either after you received the loan disbursement or the first pay period after receiving the loan.

The PPP Flexibility Act gives you 24 weeks to use your PPP loan. This covered period extension gives you more time to spend your PPP loan and receive loan forgiveness.

If you received your loan before the PPP Flexibility Act was signed into law (June 5), you can still elect to use the eight-week covered period if you prefer.

3. FTE reduction exemption

Using the PPP loan on eligible expenses isn’t the only requirement for getting your loan forgiven. You must also keep your full-time equivalent (FTE) employee numbers up to avoid forgiveness reduction.

However, the PPP Flexibility Act is a bit more understanding of employers’ responsibilities during the coronavirus pandemic.

You may be exempt from the FTE loan forgiveness reduction if you:

- Can’t rehire individuals who were employees on February 15, 2020 and can’t hire similarly qualified employees for empty positions before January 1, 2021 OR

- Can show how complying with the CDC’s, OSHA’s, or Secretary of Health and Human Services’ health guidelines (e.g., social distancing) between March 1, 2020 – December 31, 2020 prevented you from being able to return to the same level of business activity you had before February 15, 2020

To qualify for this FTE reduction exemption, you must certify in good faith and provide documents to back up your claims.

4. Loan repayment deferral period

Under the original PPP guidelines, borrowers whose loan was partially or fully unforgivable did not have to make any loan payments for six months.

Now, the loan repayment deferral period has been extended until one of the following (whichever is earlier):

- The date the SBA remits the forgiveness amount to the borrower

- 10 months after the end of the covered period (if the borrower doesn’t apply for forgiveness)

5. Loan term

Originally, the CARES Act established a loan term of two years at an interest rate of 1% for borrowers who must repay part or all of their PPP loan.

The Paycheck Protection Program Flexibility Act extends this loan term to five years. The interest rate of 1% remains the same.

6. Payroll tax deferral

Under the CARES Act, all employers could defer the employer portion of Social Security tax … unless you were a PPP borrower whose loan was forgiven.

But now, the payroll tax deferral is a universal benefit for all employers, regardless of whether your PPP loan is forgiven or not. You can defer paying your 2020 employer Social Security taxes for the entire year.

Be sure to still pay your deferred Social Security taxes by the following dates:

- December 31, 2021 (50%)

- December 31, 2022 (remaining amount)