One of your first decisions as a small business owner is choosing between business structures. Your structure dictates many vital aspects of your company, including liability. To protect your personal assets from business liabilities, you may consider structuring as a corporation.

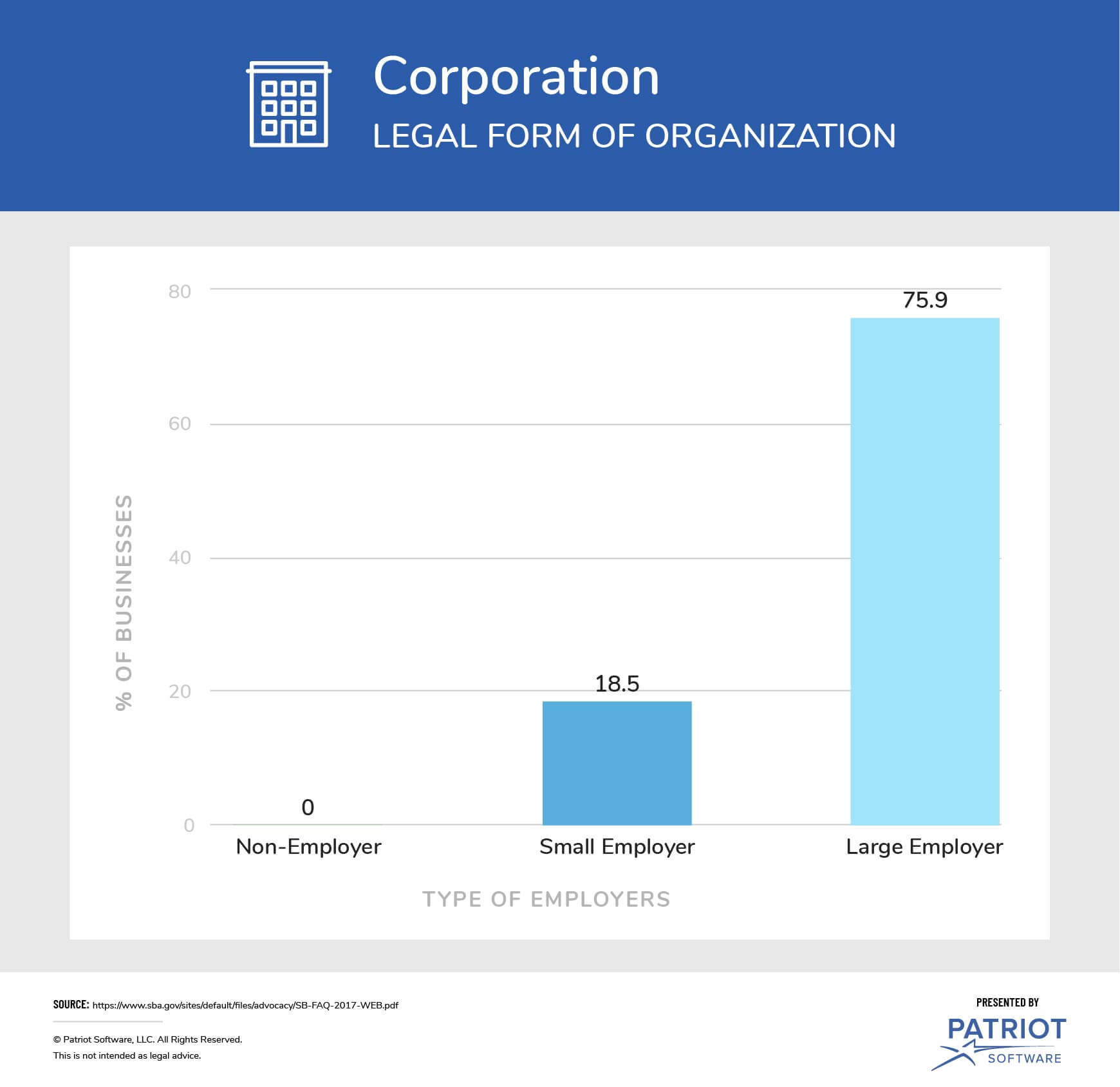

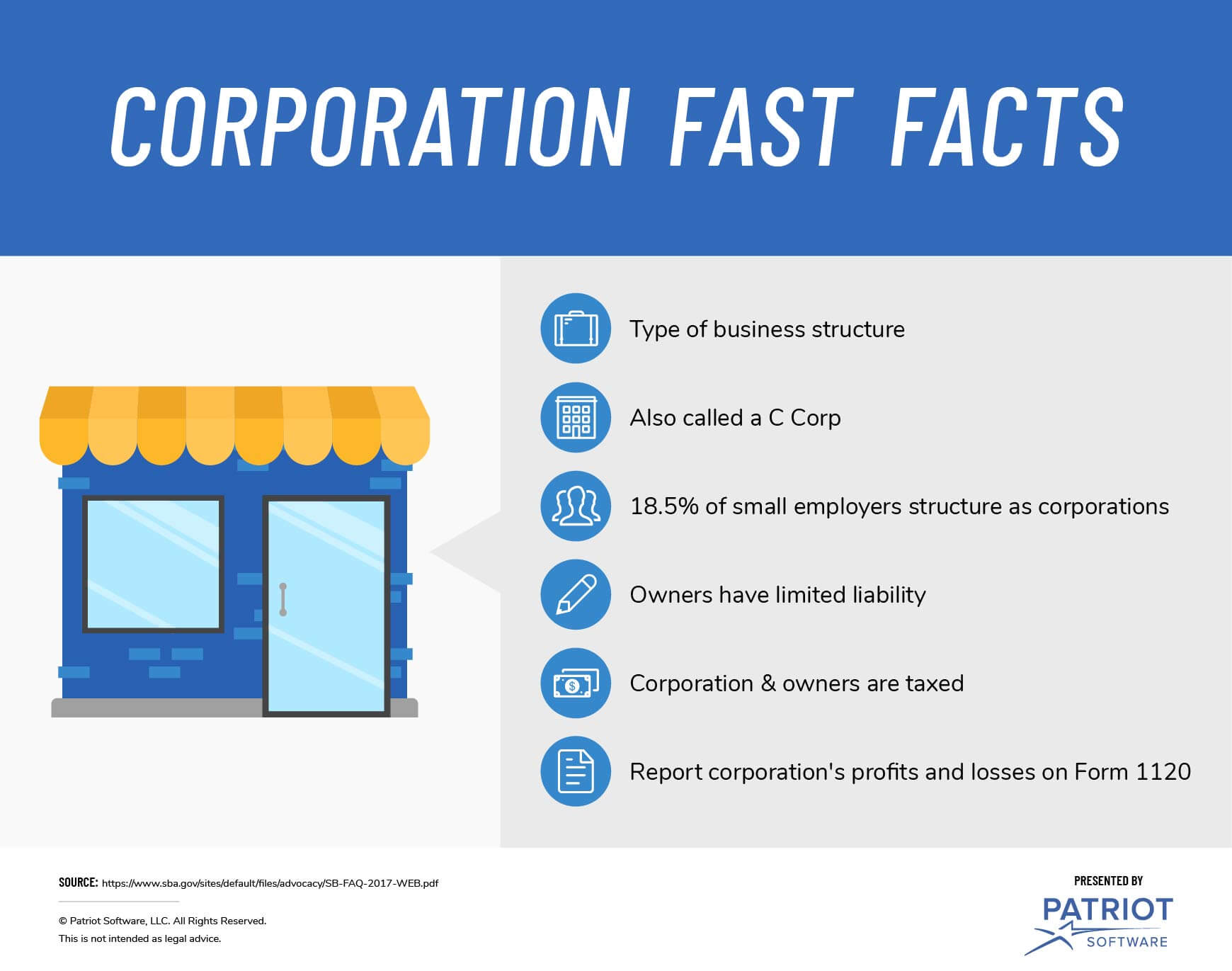

According to the Small Business Administration, 18.5% of small employers structure as corporations. What is a corporation, and why would you want to form one?

What is a corporation?

A corporation, or C Corp, is a type of business structure that is a separate legal entity from its owners. Corporation owners, also called shareholders, enjoy limited liability. Through limited liability, owners are not personally liable for the business’s actions and debts.

Because a corporation is a separate entity, it can enter into contracts, own assets, be sued, and have loan agreements.

Being a separate legal entity also means corporations are responsible for paying taxes. As a result, corporations and business owners are taxed twice.

C corporation taxes

The tax implications of incorporating your business as a C Corp are more complicated than other business structures.

First, corporations themselves are taxed. The business pays a corporate income tax rate on its profits. With the passage of the 2017 Tax Cuts and Jobs Act, the corporate income tax rate dropped from 35% to the new rate of 21%.

After the corporation is taxed, owners are also taxed. If you earn a salary, you pay taxes at your personal income tax rate. If you receive dividends, you are taxed at the dividend tax rate.

To pay corporation taxes, you must apply for a federal employer identification number (FEIN). An FEIN is a type of taxpayer identification number. The IRS requires corporations to have their own tax ID numbers because they are separate entities. You must include the identification number on company documents and tax returns.

How to incorporate

Before incorporating, keep in mind that corporations have higher administrative fees than other types of business structures. Structuring as a corporation can be expensive and time consuming, making it a better structure choice for established businesses.

You can incorporate regardless of whether you are the only owner or have hundreds of co-owners.

If you decide to incorporate your business, you must follow your state’s laws. Each state sets laws and fee structures that corporations must follow.

Generally, you must do the following to form a C Corp:

- Register your company’s legal business name with your state

- Appoint directors and officers (e.g., CEO) for your business

- File articles of incorporation with your state

- Issue stock (ownership in the company) certificates

- Apply for an FEIN

- Apply for business licenses and permits

- Establish a founders’ agreement (if applicable)

For more information on what you need to do to incorporate, check with your state government.

C Corp filing

To report your corporation’s profits and losses, file Form 1120, U.S. Corporation Income Tax Return. Filing Form 1120 fulfills your corporation’s tax responsibilities. You will also need to report your income on your personal tax return.

Generally, the C Corp filing deadline is April 15.

C corporation alternatives

Corporations are only one type of business structure you can choose. Other business entities include sole proprietorships, partnerships, limited liability companies, and S corporations.

C Corps vs. S Corps

C Corps aren’t the only type of corporations available. You can also structure as an S Corp. Like a corporation, S Corps are separate legal entities from their owners. Unlike regular corporations, S Corp owners enjoy pass-through taxation, meaning they only pay taxes on their personal income.

You can form an S Corp if you are incorporated. After establishing a C Corp, file Form 2553, Election by a Small Business Corporation, to elect S Corp status.

Before you file Form 2553, keep in mind that the IRS sets strict requirements on which businesses can be S corporations. For example, you must have 100 or fewer owners to form an S Corp.

As a business owner, you are responsible for recording your company’s profits and losses. With Patriot’s online accounting software, you can easily record transactions and keep your books up to date. Plus, we provide free, U.S.-based support. Try it for free today!

This article has been updated from its original publication date of 08/18/2016.

This is not intended as legal advice; for more information, please click here.