If you run a nonprofit organization, your accounting responsibilities are different than those of for-profit businesses. Nonprofit organizations handle tax payments, financial statements, and recordkeeping differently than other businesses. Learn about nonprofit accounting below.

What is considered nonprofit?

A nonprofit organization operates to fulfill a charitable, educational, religious, or scientific purpose, rather than to earn profits. Although nonprofits do need revenue to operate, earning profits is not their primary function.

Many nonprofits receive tax-exempt status. If you qualify for tax-exempt status, you are not required to pay federal business income taxes. However, you might still need to pay state and local income taxes. Not all nonprofits are tax exempt. Tax-exempt nonprofits are known as 501(c)(3) organizations.

Nonprofit accounting

Whether you’re thinking about starting a nonprofit or already have, understanding the unique aspects of accounting for nonprofit organizations is essential.

1. Choose an accounting method

Like for-profit businesses, nonprofit bookkeeping relies on choosing an accounting method to record incoming and outgoing money.

Like any business, your nonprofit needs a healthy cash flow to run. You need to earn enough money to pay things like employee wages, unexpected expenses, utility bills, rent, etc.

Although you might not sell products like the typical business, you have many sources of revenue. You might have members who pay dues or donors who contribute money. And, you may host fundraising events to bring in revenue.

You must record all incoming revenue and outgoing payments with an organized accounting system. You can choose a cash-basis or an accrual accounting system for nonprofit organization.

Cash-basis accounting is a system where you record expenses or income when you actually pay or receive them, not when the transaction takes place. For example, you run a nonprofit where members must pay dues. Using the cash-basis accounting system, you record payment when you actually receive dues from members. However, you cannot use this method if you make more than $5 million in annual gross sales or more than $1 million in gross receipts for inventory sales, or if you extend credit.

Accrual accounting is when you record transactions when they actually take place. This method uses a double-entry bookkeeping system. If your nonprofit collects membership dues, you would record income when you send the invoice, even though you haven’t physically received money.

2. Understand tax responsibilities

If you apply and qualify for tax-exempt status, you do not need to pay federal income taxes. And, you might also be exempt from sales and property taxes if you have tax-exempt status.

You must apply for tax-exempt status by filing Form 1023, Application for Recognition of Exemption Under Section 501(c)(3) of the Internal Revenue Code. Then, the IRS will decide if you qualify based on whether you are a “charitable” organization.

Being exempt from federal income taxes does not necessarily exempt you from filing an annual small business tax return. You are still required to report revenue and expenses to the IRS. Keep accurate records of and report your activities and finances for the year.

Unless you are not required to file a return (e.g., a church), you must file Form 990, Return of Organization Exempt from Income Tax or Form 990-EZ. Your form is due on the 15th day of the fifth month after your accounting period ends.

3. Create the appropriate financial statements

In nonprofit accounting, you should create financial statements to report your business’s finances.

For-profit businesses use three main financial statements, which are income statements, balance sheets, and cash flow statements. Nonprofit businesses use similar financial statements, but they have different names and are organized differently.

Nonprofit accounting relies on using the statement of financial position (balance sheet), statement of activities (income statement), and cash flow statement.

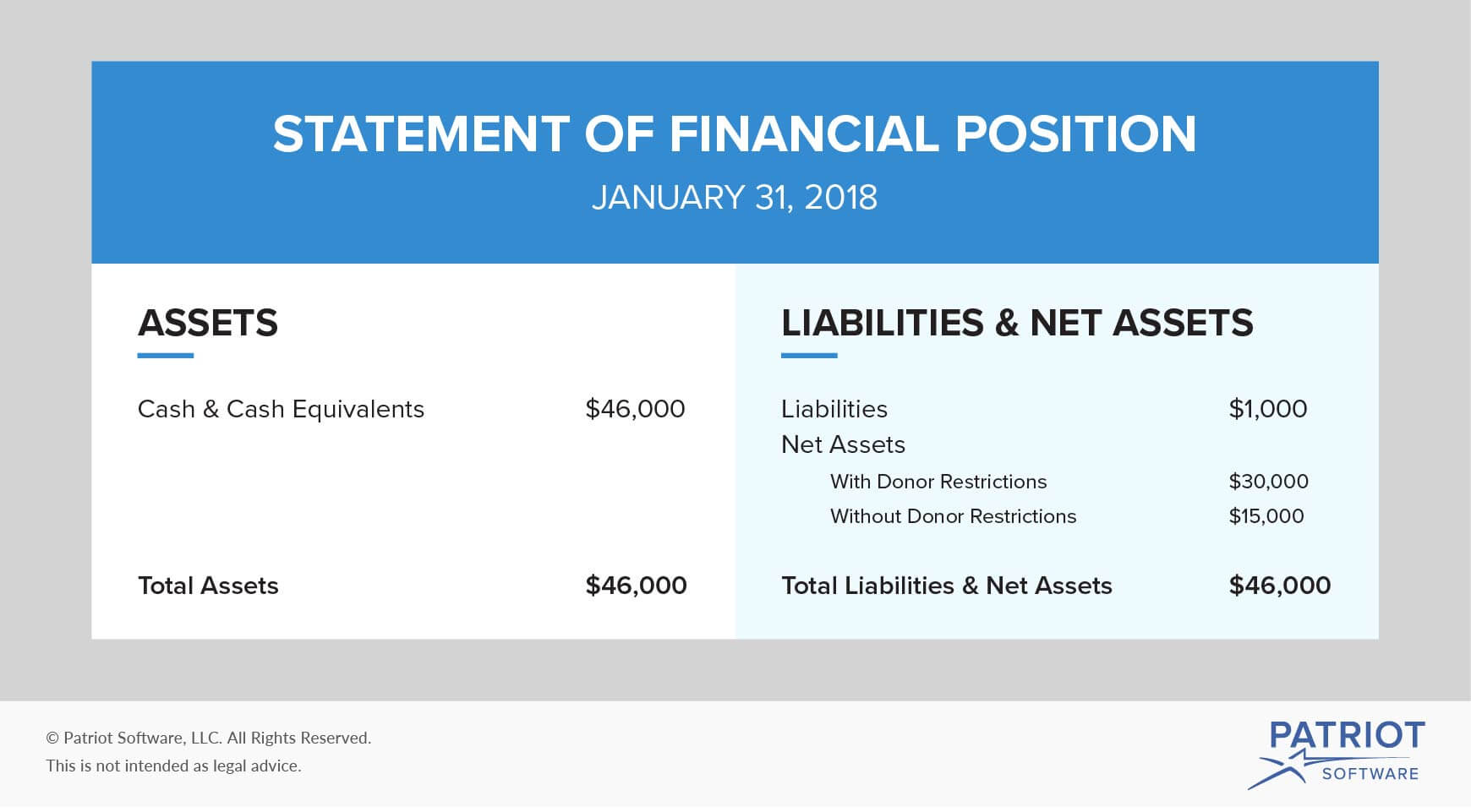

The statement of financial position gives you a screenshot of the health of your nonprofit during a period of time. The statement shows your assets, liabilities, and net assets. Unlike the balance sheet, the nonprofit version substitutes net assets for equity. Your net assets plus liabilities must equal your assets on the statement of financial position.

Net assets are classified in one of two ways: with donor restrictions or without donor restrictions. If donors make donations for specific purposes, you must label them as “with donor restrictions.”

Here is an example statement of financial position:

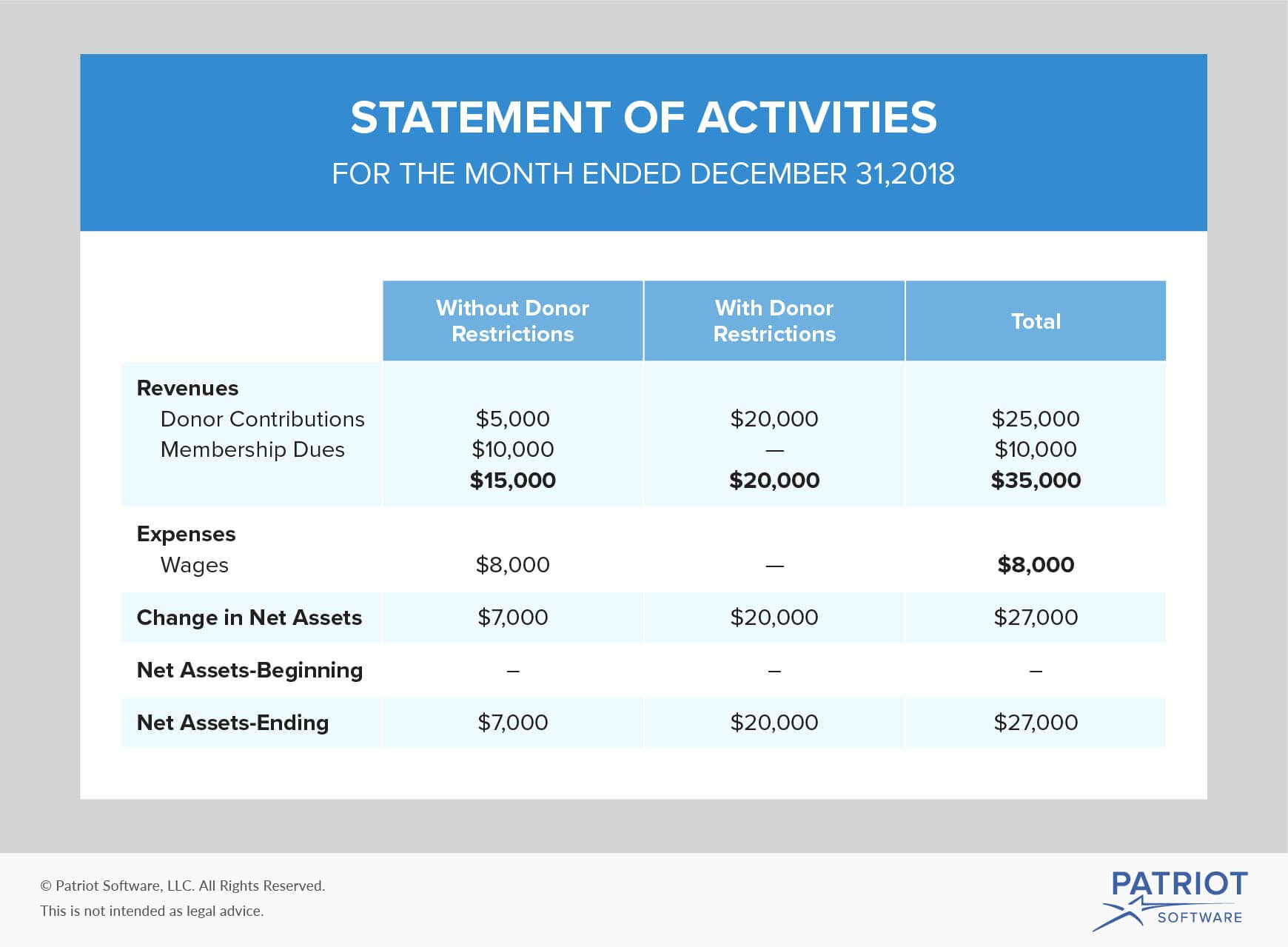

The statement of activities works similarly to the income statement. Its purpose is to report revenue and expenses during a period of time. Like the statement of financial position, you must report revenues with or without donor restrictions.

Here is an example statement of activities:

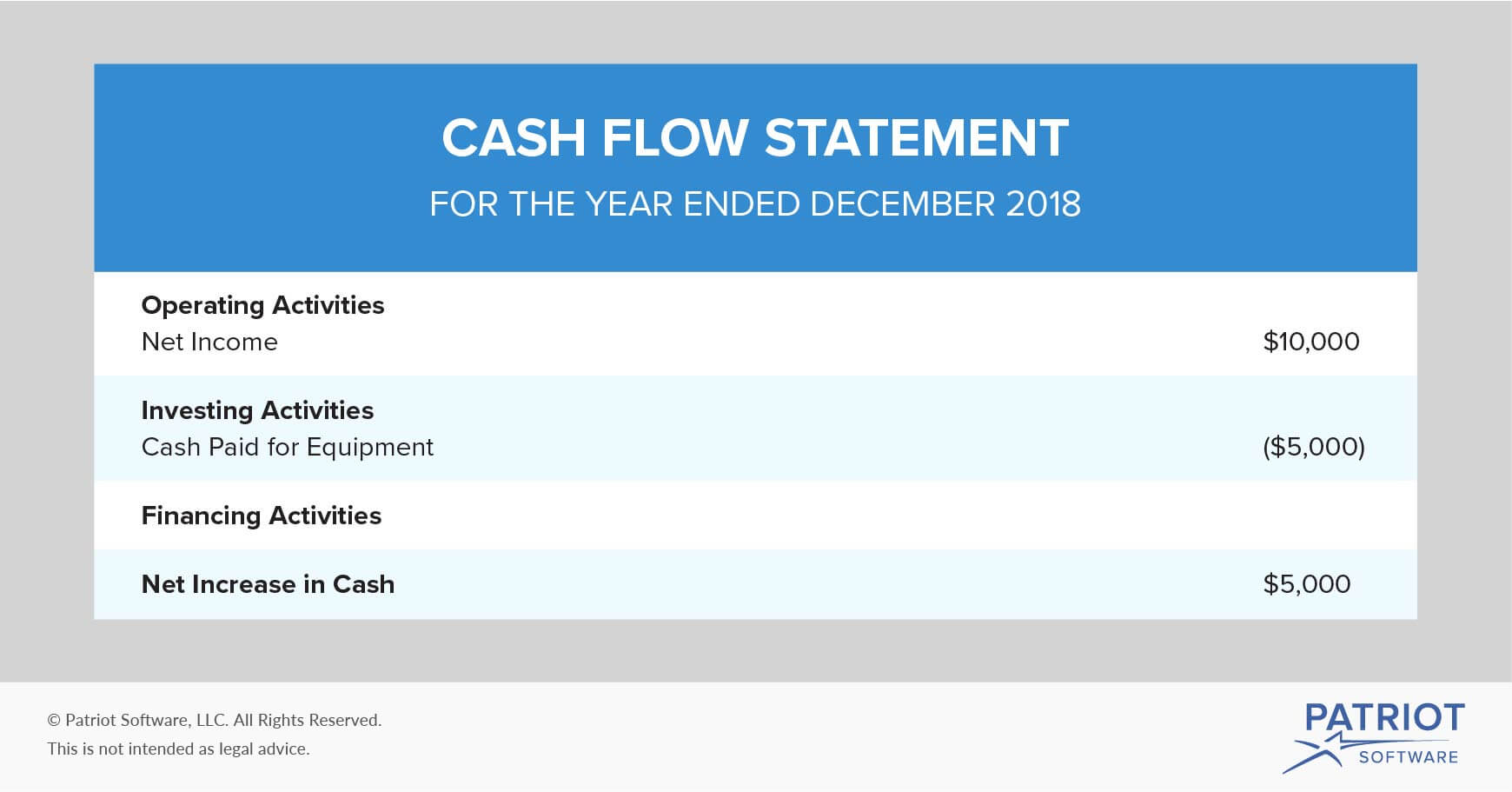

Lastly, the cash flow statement shows you how much money is entering and leaving your organization during a specific time period. The cash flow statement organizes cash into three categories, which are operating, investing, and financing activities. You can have either positive or negative cash flow in your nonprofit.

Take a look at this cash flow statement example:

Nonprofit accounting can get tricky. Use Patriot’s online accounting software to keep your books organized and up to date. Our software is made for the non-accountant, and we offer free, U.S.-based support. Give us a try today!

This is not intended as legal advice; for more information, please click here.