‘Tis the season for purchase returns … all year long. Because if you sell products at your business, you know that not all customers are satisfied. If a customer wants to bring back an item, you need to make sales returns and allowances journal entries.

Returns are a normal part of running a business. But if you don’t know how to account for a return with a purchase returns and allowances journal entry, your books will be inaccurate.

Not quite sure how to do it? That’s where your friends at Patriot come in. We’ll walk you through the process—step by step.

What is a purchase return?

A purchase return, or sales return, is when a customer brings back a product they bought from a business, either for a refund or exchange. No matter how great your products are, you’re bound to have purchase returns at some point or another.

A customer might return an item for several reasons. Maybe the customer:

- Bought more than they needed

- Bought the wrong product

- Found a better-priced good elsewhere

- Received the wrong good

- Received a damaged good

How you handle purchase returns depends on your small business return policy. You might offer free returns, charge a restocking fee, accept returns only with a receipt, or not accept returns at all. Or, maybe you decide to compensate customers returning items with store credit.

In most cases, the customer receives a refund when they physically return the good. You can also lay out a return time frame in your payment terms and conditions.

OK, so those are the basics of what sales returns are. Now onto the recordkeeping part—accounting for the return in your books…

The basics of sales returns and allowances

When a customer buys something for you, you (should) record the transaction in your books by making a sales journal entry. So, when a customer returns something to you, you need to reverse these accounts through debits and credits.

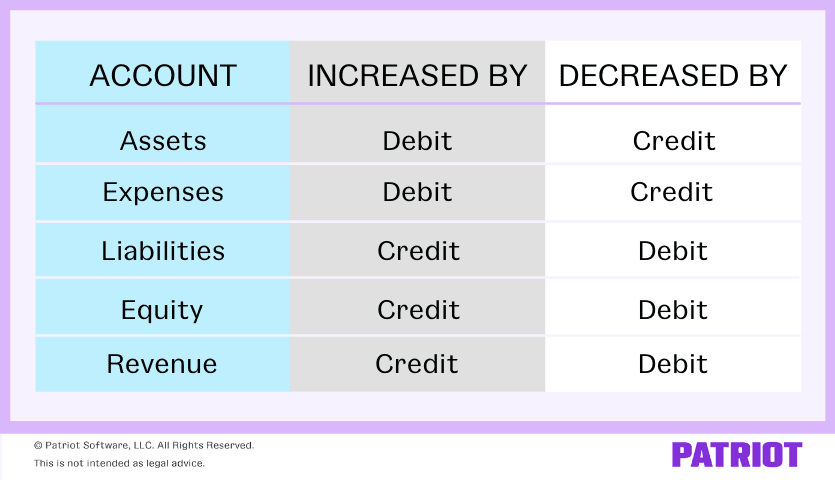

Debits increase some accounts and decrease others. The same is true for credits. Debits and credits are equal and opposite, so when you increase an account using a debit, you must decrease another with a credit.

You can use the following chart to see how debits and credits impact each account:

So, what is the purchase return account you need to know about? Well, there are a few accounts you may be dealing with when a customer returns merchandise:

- Sales returns and allowances

- Cash

- Accounts payable

- Accounts receivable

- Inventory

- Cost of goods sold

Creating a sales return and allowances journal entry

Accounting for sales returns can be tricky. But, don’t be overwhelmed by debits and credits. Once you get the hang of which accounts to increase and decrease, you can record purchase returns and allowances in your books.

Your responsibilities depend on how the original purchase was made and how you plan on reimbursing the customer.

But, regardless of how the customer paid, one thing remains the same: you need to update your Sales Returns and Allowances account. This account represents returned goods at your business.

The Sales Returns and Allowances account is a contra revenue account, meaning it opposes the revenue account from the initial purchase. You must debit the Sales Returns and Allowances account to show a decrease in revenue.

Ready to account for a purchase return in your accounting books?

Purchase returns for when a customer paid cash

If your customer paid in cash, you physically received the money at the point of sale. So now, you need to decide how you’re refunding the customer: cash or credit?

Cash refunds

So, you’ve decided to give the customer back the money they used to pay for your product. You already know that you need to debit your Sales Returns and Allowances account. Now, which account to credit?

If a customer made a cash purchase, decrease the Cash account with a credit. This purchase allowance journal entry lowers your net sales.

Your sales returns and allowances journal entry should look like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Sales Returns and Allowances | Sales return | X | |

| Cash | X |

Store credit

Rather than refunding a customer with cash, you might credit merchandise at your business. Accounting for a purchase return with store credit is similar to a cash refund. But instead of entering in your Cash account, you credit your Accounts Payable account.

Because you are not immediately paying the customer, you must increase the amount you owe through an Accounts Payable entry. This increases your liabilities.

Your sales returns and allowances journal entry should look like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Sales Returns and Allowances | Sales return | X | |

| Accounts Payable | X |

Sales returns for when a customer used store credit

If a customer originally made their purchase on credit, the sale was part of your accounts receivable, which is money owed to you by customers.

Recording a purchase return for a sale made on credit is a little different than when a customer pays cash.

If the customer’s original purchase was made using credit, you recorded the original sale by increasing your Accounts Receivable account through a debit.

When a customer returns something they paid for with credit, your Accounts Receivable account decreases. Reverse the original journal entry by crediting your Accounts Receivable account. Although you don’t lose physical cash, you lose the amount you were going to receive.

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Sales Returns and Allowances | Sales return | X | |

| Accounts Receivable | X |

One more thing … Inventory

When accounting for sales returns, you should also record the increase in inventory, if applicable (e.g., if you don’t throw the good away).

To update your inventory, debit your Inventory account to reflect the increase in assets. And, credit your Cost of Goods Sold account to reflect the decrease in your cost of goods sold.

Your inventory record should look something like this:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| XX/XX/XXXX | Inventory | Sales return | X | |

| Cost of Goods Sold | X |

Looking for an easier way to track your transactions? Patriot’s online accounting software lets you record income and expenses, manage receipts and documents, and more. Start your free trial today!

This article has been updated from its original publication date of April 20, 2017.

This is not intended as legal advice; for more information, please click here.