Do you find yourself purchasing or asking an employee to buy something for your business from time-to-time? If so, you may benefit from using a petty cash fund. Learn more about what is petty cash, the purpose of petty cash, and petty cash uses for your small business.

What is petty cash?

Petty cash, or petty cash fund, is a small amount of cash your business keeps on hand to pay for smaller business expenses. Petty cash is a convenient alternative to writing checks for smaller transactions.

For example, you might send an employee to pick up office supplies, like staples or printer paper. You would use your petty cash fund to reimburse your employee for the purchase of the supplies.

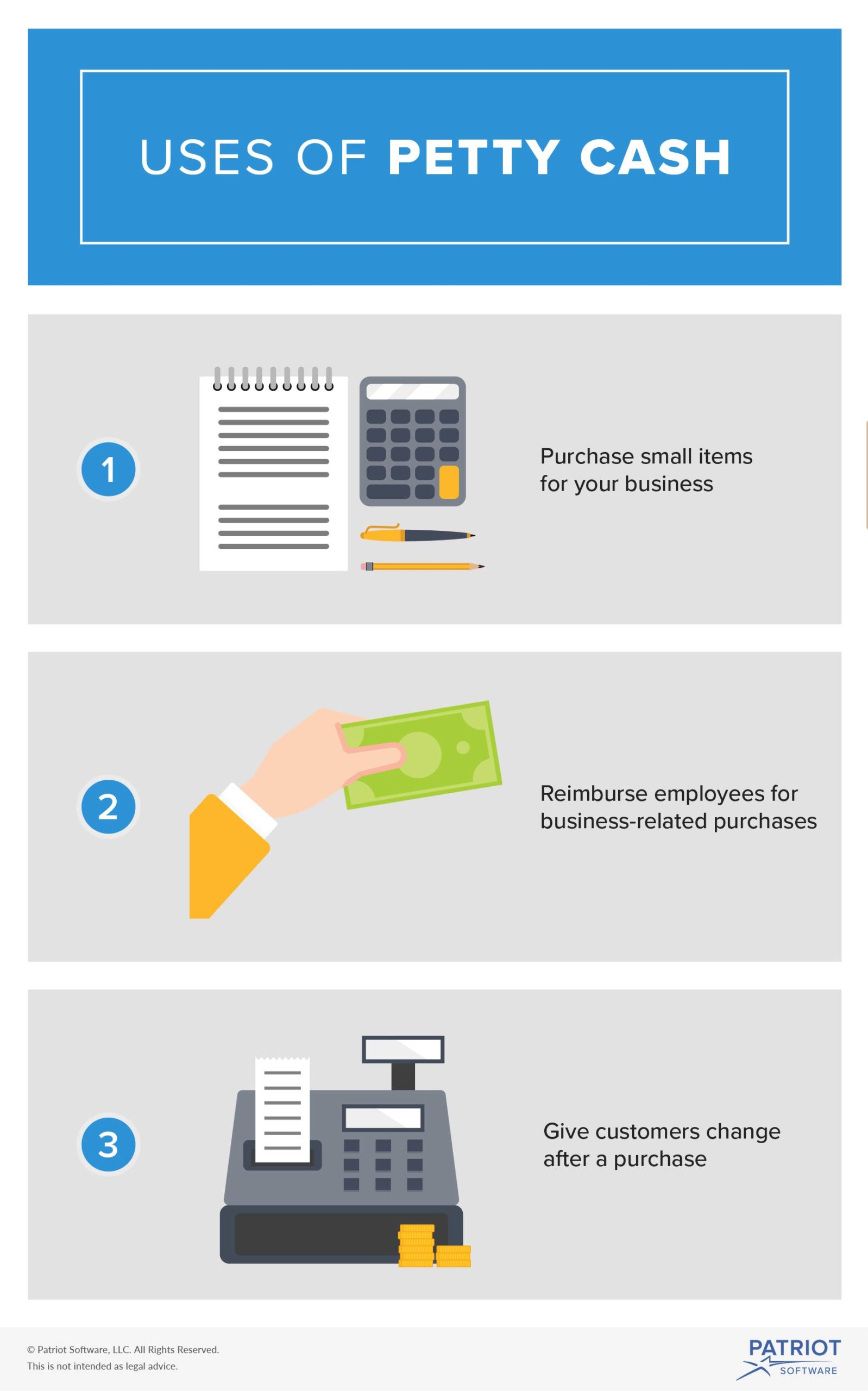

What is petty cash used for?

You can use petty cash for any small purchase. Petty cash usage ranges anywhere from buying a stamp to having bagels delivered for an early morning meeting.

Using petty cash saves you time from writing out and using up your checks. And, some vendors don’t accept debit or credit card purchases for payments under a certain dollar amount.

How large are petty cash funds?

The amount kept in a petty cash fund varies for each business. For some, $50 may be sufficient. Others might have $200 in their petty cash fund. Petty cash funds typically depend on how frequently your business makes small purchases.

Most businesses will reserve enough cash in their fund to meet their monthly needs. However, keeping too much cash could result in unused funds sitting in an account.

As your business grows, you may need to re-evaluate the amount you keep in your petty cash fund. Increase and decrease your funds as needed.

Petty cash accountability

A designated employee, the petty cash custodian, accounts for your business’s use of petty cash. When an employee takes money from the petty cash fund, the petty cash custodian must record who took the money, the amount taken, what the money is for, and the date.

An employee using petty cash should provide a receipt for the purchase to the petty cash custodian. Give the receipt to your finance department or the person who handles your small business books.

You typically evaluate your petty cash fund at the end of each month for more accurate balances. Remember to record petty cash expenses in your accounts as journal entries.

Petty cash do’s and don’ts

Review petty cash do’s and don’ts to ensure you correctly handle your fund.

You must specify what the petty cash can be spent on. Make sure your employees understand what the petty cash fund can or can’t be used for by creating a petty cash policy.

Designate a reasonable amount for your petty cash fund. Establishing a dollar amount to meets your business’s petty cash needs is essential. When your petty cash fund gets low, you must refill it. You don’t want to replenish the balance too often. And, you don’t want the amount to be too high in case of theft.

Don’t give petty cash access to every employee. Your petty cash custodian should be the only employee distributing petty cash. Your petty cash custodian determines if the expense is appropriate according to your business’s petty cash policy.

Petty cash is considered a highly liquid asset. Employees or customers can easily steal your cash. Don’t leave your petty cash fund unsupervised. Consider keeping your petty cash locked in a drawer, safe, or filing cabinet.

Petty cash and taxes

Since most petty cash purchases are for business expenses, you will likely be able to deduct them from your business’s taxes at year-end.

Keep and record every receipt for petty cash purchases. You must document each expense if you want to deduct it from your business taxes. If you don’t document your petty cash purchases, you will not be able to deduct the expenses when you pay business taxes.

Review IRS Publication 583 for more petty cash requirements and recommendations for recordkeeping.

Need a simple, affordable way to keep your petty cash records? Patriot’s accounting software allows you to easily manage incoming and outgoing money. Try it for free today!

This article was updated from its original publication date of 12/5/2014.

This is not intended as legal advice; for more information, please click here.