To start, operate, and grow a business, you most likely need to take on some form of debt. Many business owners have revolving and installment debts to fund their companies. In order to make smart financing decisions, you must understand the difference between revolving debt vs. installment debt.

Revolving debt vs. installment debt

As a business owner, you need to learn when to take on installment debt vs. revolving debt. Using each form of debt at the appropriate time can lead to better small business credit scores, lower monthly payments, and more repayment flexibility.

First, you need to learn about both forms of debt.

What is revolving debt?

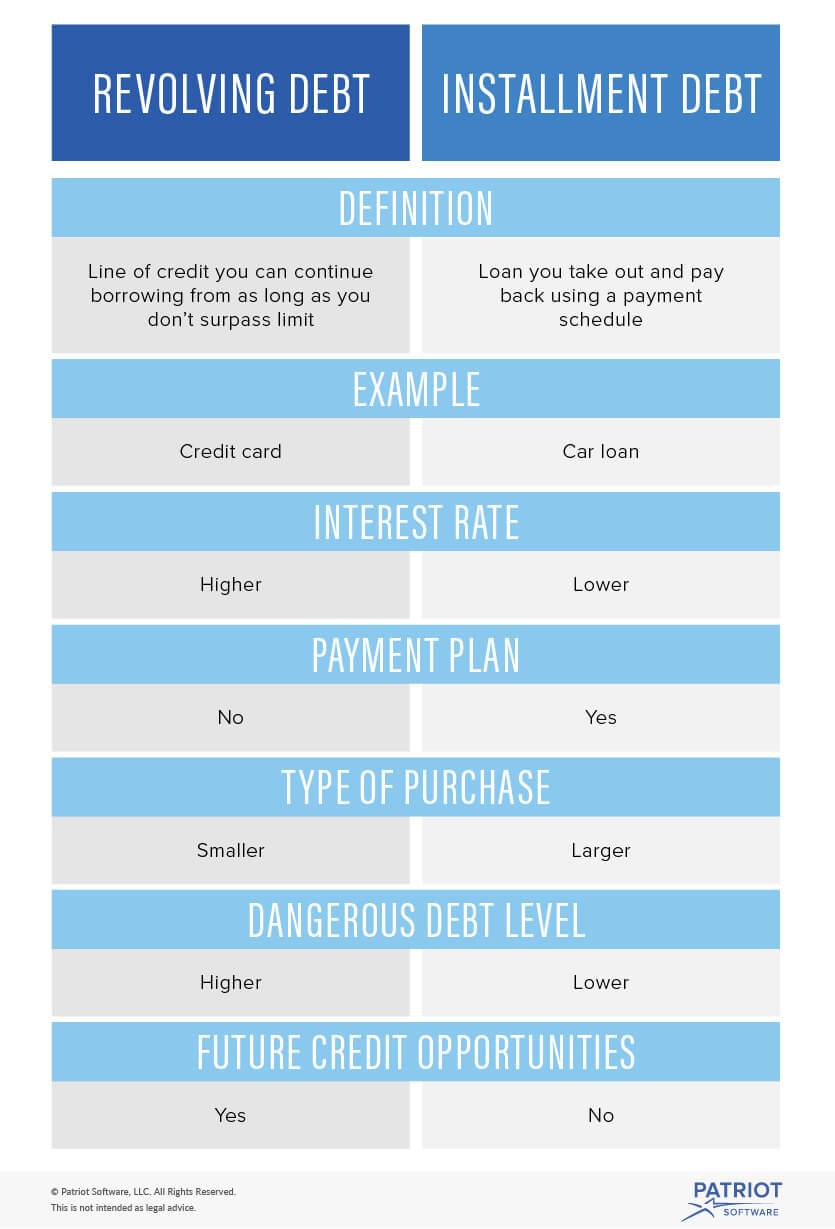

Revolving debt is a line of credit that does not require a payment plan. It is a flexible financing method that lets you continue borrowing from your line of credit as long as you do not go over your limit.

You must repay what you spend out of your revolving debt, plus interest. If you don’t use all of your credit line, you do not need to repay it. There is no payment plan, so you make payments based on what you can afford. The balance decreases each time you make a payment. You can choose to borrow more money from your revolving line of credit.

Once you’re approved for the line of credit, you don’t need to keep reapplying. You can continuously use your revolving credit line as long as you don’t go over the limit. With installment loans, you must apply each time you want a loan.

You can also use revolving debt for small purchases that help with business operations. For example, you have a ceiling leak that costs $400 to fix. You can use your revolving debt to cover the cost.

Examples of revolving debt include the following:

- Credit cards

- Retail cards

- Home equity lines of credit

Revolving debt example

You have a revolving line of credit for $5,000. You purchase a new laptop for $500. Now, you only have $4,500 left on your line of credit. You must pay back the $500 with an interest rate of 20%.

Original revolving debt: $500

Simple interest: 20%

Remaining line of credit: $4,500

Total owed: $600

$500 X .20 = $100

$500 + $100 = $600

What is installment debt?

Installment debt, or term debt, is a loan you take out and pay back using a payment schedule. Each payment you make goes toward the original loan plus interest. There might be additional charges, like a setup fee and processing fees.

With each payment you make, the balance decreases. After using the loan amount, you cannot continue to borrow more money, which is different than revolving debt.

There is a set length of the loan. Your lender tells you when the loan term ends. Installment debt is predictable because your month-to-month payment liability typically does not change.

Here are some popular installment loans:

- Small business loans

- Equipment loans

- Mortgages

- Car loans

- Student loans

Installment debt example

For example, you take out a loan for $5,000 to fund a new copy machine. You have a simple interest rate of 10%. Your loan term is 24 months.

Original installment loan: $5,000

Simple interest: 10%

Loan term: 24 months

$5,000 X .10 = $500

$5,000 + $500 = $5,500

$5,500/24 = $229.17

You must make monthly payments of $229.17 for two years to cover the interest and the loan. This installment loan makes it possible to make large purchases with lower interest rates (generally) than revolving credit.

When to use revolving credit vs. installment credit

Determining when to use revolving credit vs. installment credit doesn’t have to be difficult. When you need to make smaller purchases on short notice, it’s best to use revolving credit. For large expenses, installment debt is the better option.

Interest rates are higher for revolving debt than installment debt. In fact, interest rates for revolving debt can be 15-20% more than installment debt. Try to pay off revolving debt quickly and stay away from accumulating too much debt.

Tips

When you make payments with installment purchases, make sure you stick to the payment plan. You can make larger payments each month, but check to see if there is a penalty for paying off the loan early. With revolving credit, it’s best to pay it off as soon as you can since interest rates are high.

Need a way to track your business’s money? Patriot’s online accounting software lets you track expenses so you can account for your business debts. And, we offer free, U.S.-based support. Get your free trial today!

This is not intended as legal advice; for more information, please click here.