When you’re in business, you’re bound to deal with credit and loans. So, are you extending credit to customers, requesting credit, borrowing a loan from lenders, or doing all of the above? If so, you need to know about the Consumer Credit Protection Act.

What is the Consumer Credit Protection Act?

The Consumer Credit Protection Act (CCPA) is a federal law established in 1968 to protect consumer rights when dealing with lenders. There are a number of provisions that were enacted under the CCPA, including the Truth in Lending Act (Title I), Federal Wage Garnishment Law (Title III), Fair Credit Reporting Act (Title VI), Equal Credit Opportunity Act (Title VII), and the Fair Debt Collection Practices Act (VIII).

Title I of the Consumer Credit Protection Act, the Truth in Lending Act (TILA), requires that lenders and creditors disclose pertinent information to borrowers, like interest rates and total costs.

Title III of the CCPA protects employees whose wages are subject to garnishments. Under the act, employers cannot fire employees for having one garnishment. And, Title III limits the amount that can be subject to garnishments.

Title VI, Fair Credit Reporting Act (FCRA), protects consumer credit information by keeping it private. Under this act, a party cannot access credit files for individuals unless they get permission first.

Title VII, the Equal Credit Opportunity Act (ECOA), prohibits credit discrimination due to race, color, religion, national origin, sex, marital status, or age. It also prohibits discrimination against individuals receiving public assistance.

Title VIII, Fair Debt Collection Practices Act (FDCPA) of the Consumer Credit Protection Act aims to protect consumers from abusive or deceptive debt collection practices. Although this act covers debts like credit card and household debts, it does not cover business debts.

The Consumer Credit Protection Act and your business

Now that you have a little background on what the Consumer Credit Protection Act of 1968 is, you might be wondering what it has to do with your business. Fair enough.

Whether you’re the lender or the borrower, you need to know consumer protections under the CCPA. That way, you can lend legally (e.g., extending credit to customers) and borrow wisely (e.g., getting a small business loan).

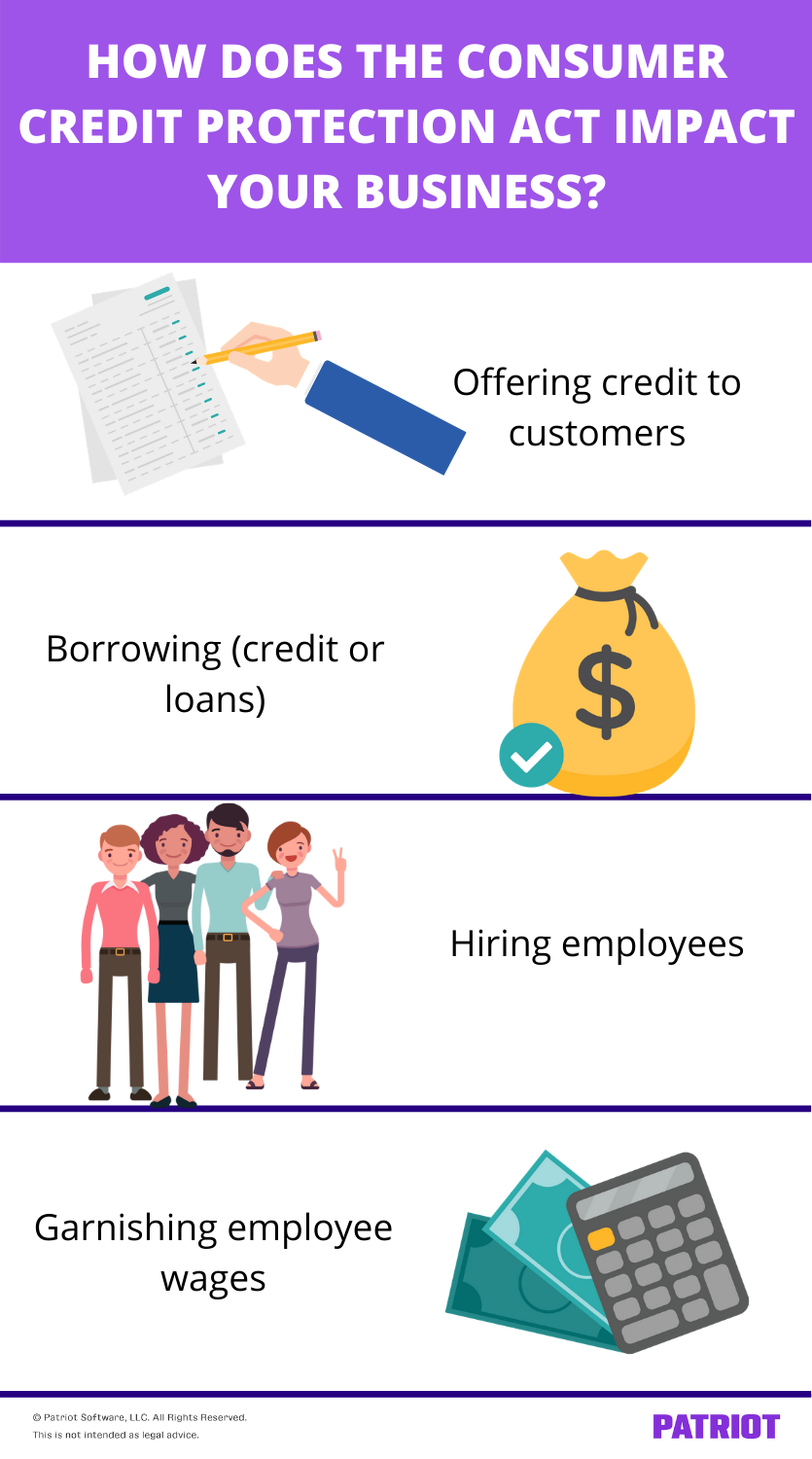

The CCPA may impact your business in a number of ways, including:

- Offering credit to customers

- Borrowing (credit or loans)

- Hiring employees

- Garnishing employee wages

Offering credit

Do you extend credit to your customers? If so, you have to do a bit more than use accrual accounting. You also need to understand and follow the Truth in Lending Act, the Fair Credit Reporting Act, and the Equal Credit Opportunity Act.

The TILA requires creditors and lenders to be clear and upfront when telling borrowers about borrowing. If you extend credit to customers, you must tell them about the total amount, annual percentage rate (APR), penalties and fees, payment schedule, and total repayment amount. Include this information in your credit policy for small business, and make sure customers sign it.

You must also follow the Fair Credit Reporting Act when running a credit check on a customer who is applying for credit. The FCRA governs what type of information a creditor can collect about a borrower. And, the FCRA may require permission before conducting a credit check.

Again, the Equal Credit Opportunity Act prevents lenders from using discriminatory practices when extending credit. The EEOA requires lenders to use the following to determine creditworthiness:

- Income

- Expenses

- Debts

- Credit history

Borrowing (credit or loans)

Are you thinking about applying for a business loan? How about a new line of credit or credit card?

If you are, you need to know what consumer credit protection you should be receiving. Borrowers must follow the TILA, FCRA, and EEOA.

When you apply for a loan from a bank or other type of lender or creditor, you are entitled to detailed information about the loan or credit. Under the Truth in Lending Act, the lender or creditor must tell you the:

- Total amount

- APR

- Fees and penalties

- Repayment plan

- Repayment amount

After you receive information about the loan or credit you’re applying for, you can make an informed decision before signing.

The Fair Credit Reporting Act entitles consumers to one free credit report every 12 months from Equifax, Experian, and TransUnion. Before applying for a new business loan or line of credit, you may want to check your credit report. Plus, when you apply for a loan or credit, you may need to give written permission to the lender to conduct a credit check under the FCRA.

Under the Equal Credit Opportunity Act, lenders cannot discriminate against you when you apply for a business loan or line of credit. Instead, they must look solely at appropriate credit-determining factors, such as credit history.

The EEOA prevents creditors or lenders from discouraging you from applying or imposing unfair terms and conditions based on a discriminatory practice.

Hiring employees

When you hire employees, part of your due diligence includes conducting a background check. And in most cases, a credit check is part of a background check.

But before you go conducting a credit check, you must comply with the FCRA. Get the potential employee’s permission before you attempt to obtain information about their credit.

Garnishing employee wages

Wage garnishment refers to an employer withholding money from an employee’s wages to repay a debt, as per a court order or other legal procedure. Employers cannot discharge employees because of garnishment for a single debt.

However, Title III of the CCPA does not prevent employers from discharging workers if their wages are subject to garnishment for two or more debts.

The act also sets a limit on the amount of money that can be garnished from a worker’s earnings per payday. Unless the garnishment is for child support or alimony, the employee’s garnishment cannot be more than either:

- 25% of their disposable earnings

- The amount that their disposable earnings are greater than 30 times the federal minimum wage

No matter your business, you need a reliable accounting method to stay on top of your books. Patriot’s accounting software makes it easy to manage your business’s books. Plus, we have a patented Dual-Ledger Accounting feature that displays your financial reports in either accounting method. Try it for free today!

This article has been updated from its original publication date of June 1, 2012.

This is not intended as legal advice; for more information, please click here.