If you have ever made a mistake in your small business financial statements, you know how time consuming and expensive errors in accounting can be. You need to protect your small business books from common accounting errors.

Different types of accounting errors

Errors in accounting happen to everyone. But, you should try to avoid them whenever possible. There are several things you can do to avoid making accounting mistakes in your books. Look out for these five types of accounting errors.

#1. Errors of omission in accounting

Whether you’re collecting customer payments or buying inventory, you constantly handle transactions. The inflow and outflow of cash sometimes cause business activities to slip through the cracks. When you forget to record transactions, they are errors of omission.

Unrecorded general business expenses can cause big problems, like throwing off your books. Inaccurate financial records create issues with measuring profitability and filing small business taxes.

It’s important to record every business transaction, even seemingly insignificant ones. Organize small expenses into the appropriate accounts and keep the receipts.

For example, petty cash is a small amount of cash you keep on hand. Most businesses use the petty cash fund to pay for inexpensive items. If you buy something with petty cash, record it in your accounting general ledger. Neglecting to do so could lead to accounting mistakes down the road.

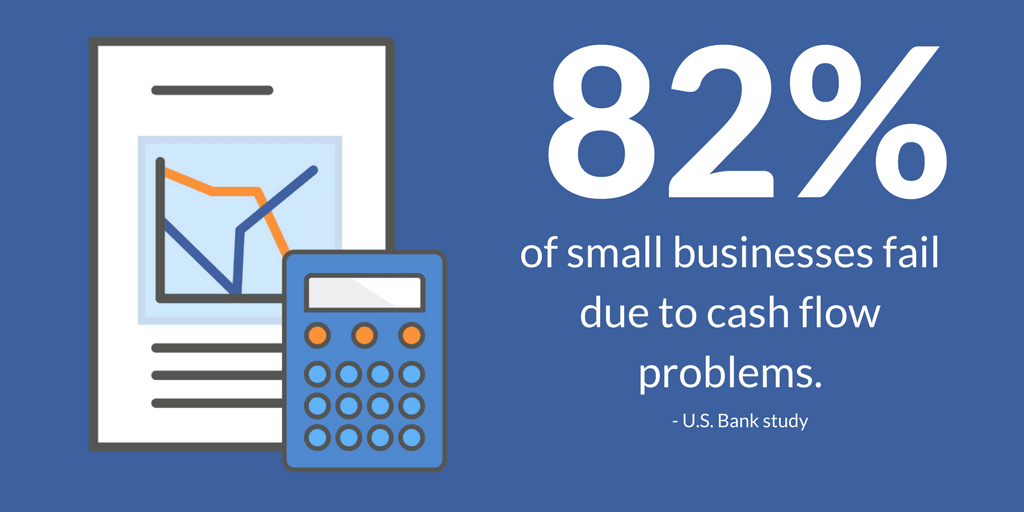

#2. Treating net profits and cash flow equally

Net profit and cash flow both have to do with income and expenses. But, there is a big difference in how net profit and cash flow measure money.

Net profit looks at whether you make money after paying expenses. To find the net profit, subtract your expenses from sales dollars. Net profit measures a specific block of time and reflects the amount of cash your business gained during a certain period.

Cash flow measures how fast you move money. Your cash flow statement shows the money coming in and going out of your business. By projecting the cash flow of your business, you can see the liquidity of your funds.

This is one of the most common accounting errors of small businesses. Why is the difference between net profit and cash flow a big deal?

Let’s say you make a $500 sale. You invoice the customer, but you don’t receive payment right away. Your books reflect the net profit earned. But, there are low available funds because you don’t immediately have the money on hand (a result of cash flow).

#3. Not reconciling your books

Reconcile your books with your bank account regularly to check for accuracy. Make sure the balances of your bank statement and accounting records match. By not reconciling, most common accounting errors can go unnoticed in your books for a long time, which makes them harder to find come tax season.

Reconciling accounts helps you catch an error of original entry early. For example, if you close the books on a monthly basis, you might notice you entered a “7” instead of a “9.” You see that your bank account balance is $2 more than the balance in your books. This is known as an error of original entry. At the time, the accounting error is a simple fix.

Imagine you did not reconcile your accounts. It takes six months to notice the error when you’re filing taxes. You have to sort through six or more months of records to find small accounting mistakes that could’ve been prevented.

#4. Failing to use a budget

If you’re like most small businesses, you’re working with limited funds. To avoid overspending, you need a strategy. You can plan for income and expenses with a business budget.

A budget helps you keep your money on track. When you create a business budget, you cut out some of the guesswork in financial planning. Use past accounting records to project future income and expenses. Try to stick to your budget once you’ve put it in place.

If you buy materials for individual customers, budget each project you do. Use the budget to charge customers and make sure you’re earning a healthy profit margin. Talk with customers about the budget before starting a project.

#5. Too much time spent on accounting

As a small business owner, you might feel like you need to do it all. Keeping the ship afloat on your own is an honorable notion. But, it’s OK to take some of the stress out of tasks that don’t generate revenue.

Managing your books is time consuming and doesn’t produce cash. You need an effective way to handle accounting so you can get back to running your business without facilitating accounting errors.

Consider finding an accountant for small business only when you need one. For example, tax season and when you expand your business are great times to work with an accountant. Accountants understand the details in your books and can advise you on important decisions.

When it comes to accounting for small business, don’t be afraid of online automation. Use accounting software to streamline your books. The software calculates account balances for you, so you can record transactions quickly.

| Want to steer clear of accounting mistakes? Download our FREE guide, Preventing Small Business Accounting Mistakes, to find out errors 6 – 10 (plus how to fix them if you make a mistake). |

You can track money in a few simple steps with Patriot’s online accounting software. Get automated and accurate records with free, U.S.-based support. Try it for free today.

This is not intended as legal advice; for more information, please click here.