When you own and operate a small business, you build up a collection of tangible and intangible assets. Tangible assets include valuable things you can touch, like your business’s building, vehicles, equipment, furniture, etc. Intangible assets are the opposite—they are not physical items. As a result, accounting for intangible assets can get tricky.

Before learning how to account for intangible assets, you need to understand what intangible assets are.

What are intangible assets?

Unlike tangible assets, intangible assets are items of value your business owns that you can’t physically touch. Intangible assets include patents, trademarks, copyrights, licenses, and other valuable items you own but cannot physically see. An example of an intangible asset would be a patent your business purchased.

Intangible assets are long-term assets. This means that they cannot be easily converted into cash within one year. However, other companies can still purchase intangible assets from you.

Accounting for intangible assets

When you have assets, you are responsible for recording their value.

Include assets on your business’s balance sheet. The balance sheet is a financial statement that displays your business’s assets, liabilities, and equity. Assets appear first on the balance sheet. Intangible assets appear after your current assets (liquid assets that can be quickly converted into cash) on the balance sheet.

When you amortize intangible assets, you must include the amortized amount on your income statement. Learn about the amortization of intangibles below.

Amortization of intangible assets

Businesses amortize their intangible assets to reduce their taxable income. What is amortization of intangible assets?

Amortization is the process of spreading out an intangible asset’s cost over a certain period of time in accounting. This paints a more realistic picture of your company’s health and helps to level out your tax liabilities throughout the useful life of intangibles.

The useful life of intangible assets is the duration it contributes to your business’s value. For example, a patent that lasts 20 years would have a useful life of 20 years.

Which intangible assets are amortized? You can only amortize intangible assets that have a finite useful life, like the patent mentioned above. Because trademarks can be renewed, businesses typically do not do trademark amortization.

To find the amortization expense, you must do three things:

- Determine the asset’s initial cost

- Know the length of the asset’s life

- Calculate the asset’s residual value (i.e., the worth of the asset when you finish using it)

The amortization formula is as follows:

Intangible assets usually do not have residual value. So to find an amortization expense, simply divide the asset’s value by its lifespan.

Let’s say you purchase a patent that lasts 14 years for $28,000. For patent amortization, record the lump expense over 14 years. When you divide the total cost by its useful life ($28,000 / 14), you get $2,000. Instead of recording $28,000 once and throwing off your books and taxes, record the amortization expense as $2,000 for 14 years.

Amortization is the same thing as depreciation. However, you amortize intangible assets and depreciate tangible assets. Labeling amortization as the depreciation of intangible assets is incorrect. Depreciation is for tangible assets only. Amortization of assets is for intangibles only.

How to record amortization expenses

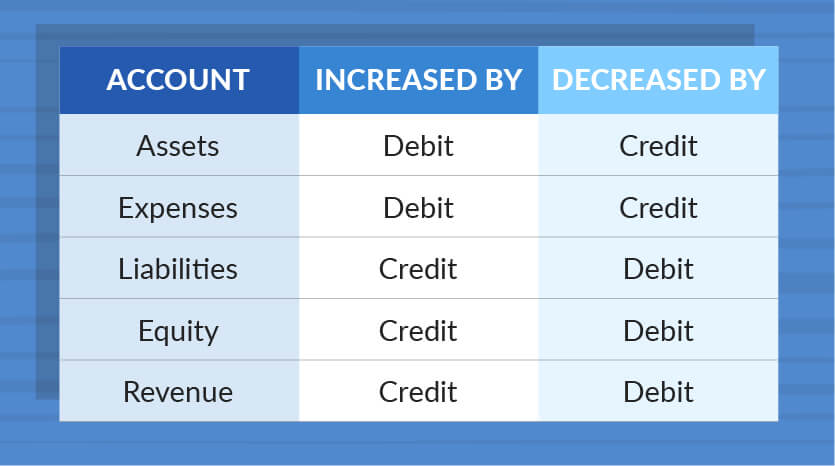

You must record amortization expenses in your accounting books. To do so, debit the amortization expense account and credit the intangible asset. This way, your entries will balance each other out.

You debit your amortization expense account because it is an expense. Expenses are increased by debits and decreased by credits. You credit your intangible asset account because it is an asset. Assets are also increased by debit and decreased by credit.

You are increasing your expenses and decreasing your assets through the amortization process. This allows you to claim your expenses and reduce your taxable income.

Using the above example, let’s say you have a patent with a useful life of 14 years that you paid $28,000 for. Your annual amortization expense is $2,000. This is how accounting for intangible assets should look in your books:

| Date | Account | Notes | Debit | Credit |

|---|---|---|---|---|

| 12/29/2017 | Amortization Expense Patent |

Patent on ABC | 2,000 | 2,000 |

How to write off intangible assets

To claim your deduction for amortization, use Form 4562, Depreciation and Amortization. You can record the amortization of your costs in Part VI of the form. For more information, visit the IRS’s website.

Keep your accounting books updated with software. Patriot’s online accounting software makes it easy to track your expenses. And, it’s made for the non-accountant. Try it for free today!

This is not intended as legal advice; for more information, please click here.