Being able to effectively manage your incoming and outgoing money ensures you have a healthy business. To do so, you need accurate financial records. Make necessary changes to your business through P&L management.

Profit and loss statement

Before talking about P&L management, you need to understand a P&L statement.

A profit and loss statement for small business is also called an income statement. It is one of the three main financial statements that businesses use to assess their company’s health. The income statement shows you your business’s profits and losses during a specific time.

A profit and loss statement is laid out by categories to show you income, costs of goods sold, gross profit, expenses, taxes, and net profit/loss.

What is P&L management?

To survive, your business needs to have more profits than losses. Too many expenses can lead to debt or even small business bankruptcy.

Profit and loss management is the way you handle your business’s profits and losses. Managing P&L means you work toward having greater revenues and fewer expenses. You use your current profit and loss statement to determine your business’s profitability.

Looking at your P&L statement can also show you where you need to make changes in your business. You can learn where you need to cut business expenses and plan ways to increase your income when managing P&L.

You need to learn how to manage P&L responsibilities. Here are some ways to get started:

1. Create P&L statements

First, create profit and loss statements. Many business owners choose to do this weekly, monthly, quarterly, or annually.

The report lays out your income and expenses in black and white. The P&L statement breaks down income and expenses so they’re easy to read. That way, you can see where your money is going each accounting period.

Creating a profit and loss statement allows you to analyze your business and make financial decisions. Also, investors and lenders use financial statements to determine whether they should give or lend you money.

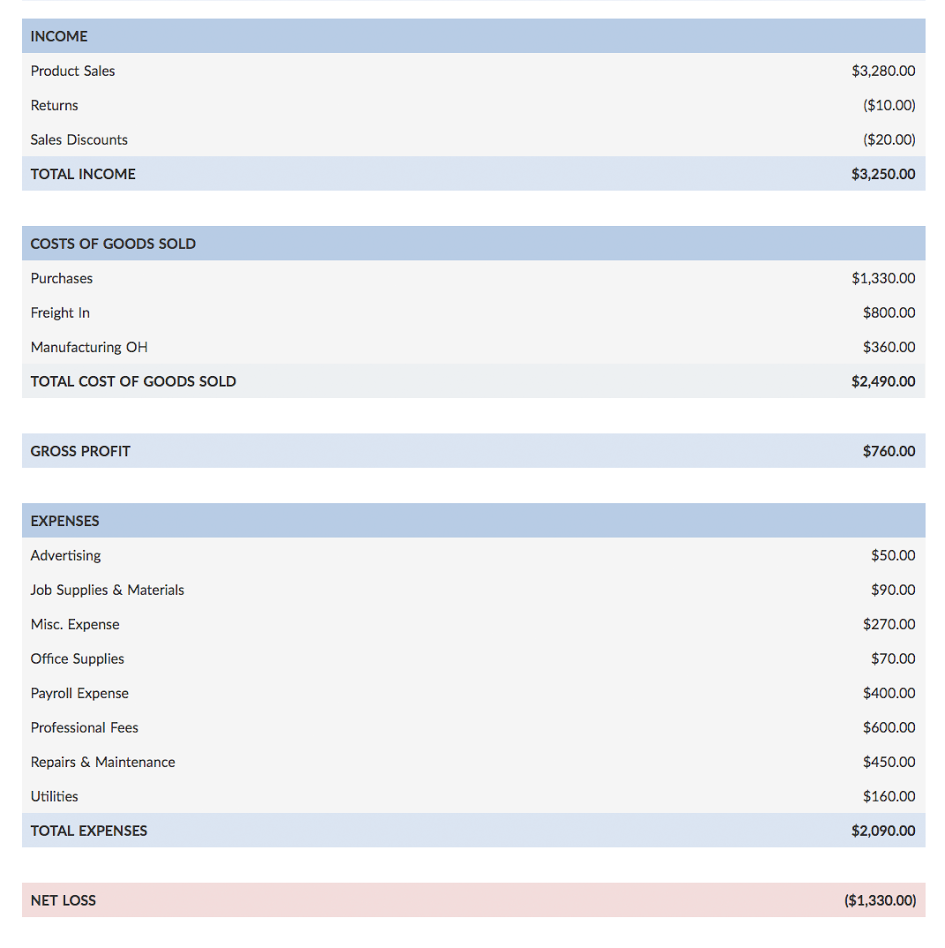

Here is an example of what a profit and loss statement looks like:

2. Compare P&L statements

Once you have your profit and loss statement for each accounting period, you can make comparisons.

Compare your current P&L statement to your past statements to determine whether your business is growing, stagnant, or declining. You can make decisions based on analyzing your statements.

For example, your January P&L statement showed a profit of $5,000, but your June P&L statement showed a loss of $1,000. Maybe you replaced a best-selling product with something else. Comparing your current and past P&L statements, along with conducting market research, might help you decide to bring back the old product.

You can also compare your P&L statement to a competitor’s. Doing so helps you locate problems within your own business. By looking at your competition’s P&L statements, you can see what areas your competitors spend money on and where they cut back.

3. Make changes to business finances

Managing profits and losses means making necessary changes to your finances. When you create and compare P&L statements, you see problems in your financial health. Recognizing these problems lets you come up with a new small business growth strategy.

You can eliminate certain expenses from your business by managing P&L. Once you see how much cash you dole out, you can shop around for new vendors to see if you can get better deals.

Sometimes, you have low cash on hand. If you extend credit, you might get customers who won’t pay you. When that happens, your business does not have as much incoming money as it should. You can adjust your invoice payment terms to get paid faster.

Managing profit and loss also means coming up with ways to make more sales. You might consider implementing strategic pricing (e.g., discounts) to draw customer traffic.

4. Meet with an accountant

Though managing profit and loss can be an internal job, it might also be good to talk with your accountant. Your accountant could help you with managing your profit and loss statement and decision-making.

If your business has losses, an accountant helps you find areas to slash expenses and manage other aspects of your money.

The importance of P&L management

If you want a healthy, growing business, you need to manage your profits and losses. Businesses that continually have more losses than profits need to make changes. You might need to adjust your payment terms, cut expenses, or make more sales.

Managing profit and loss influences your business strategies and decision-making. Grow your business through P&L management.

To measure your business’s profits and losses, you need accurate records. Patriot’s online accounting software makes it possible to track your expenses and income. We offer free, U.S.-based support. Get your free trial now!

This is not intended as legal advice; for more information, please click here.