Every year, you are required to send Form W-2 to employees by the January 31 Form W-2 filing deadline. Hopefully, those forms will get to your employees. But, some forms might come back to you as undeliverable, especially if you have incorrect employee addresses on file.

What should you do with Forms W-2 returned to employer? Find out below.

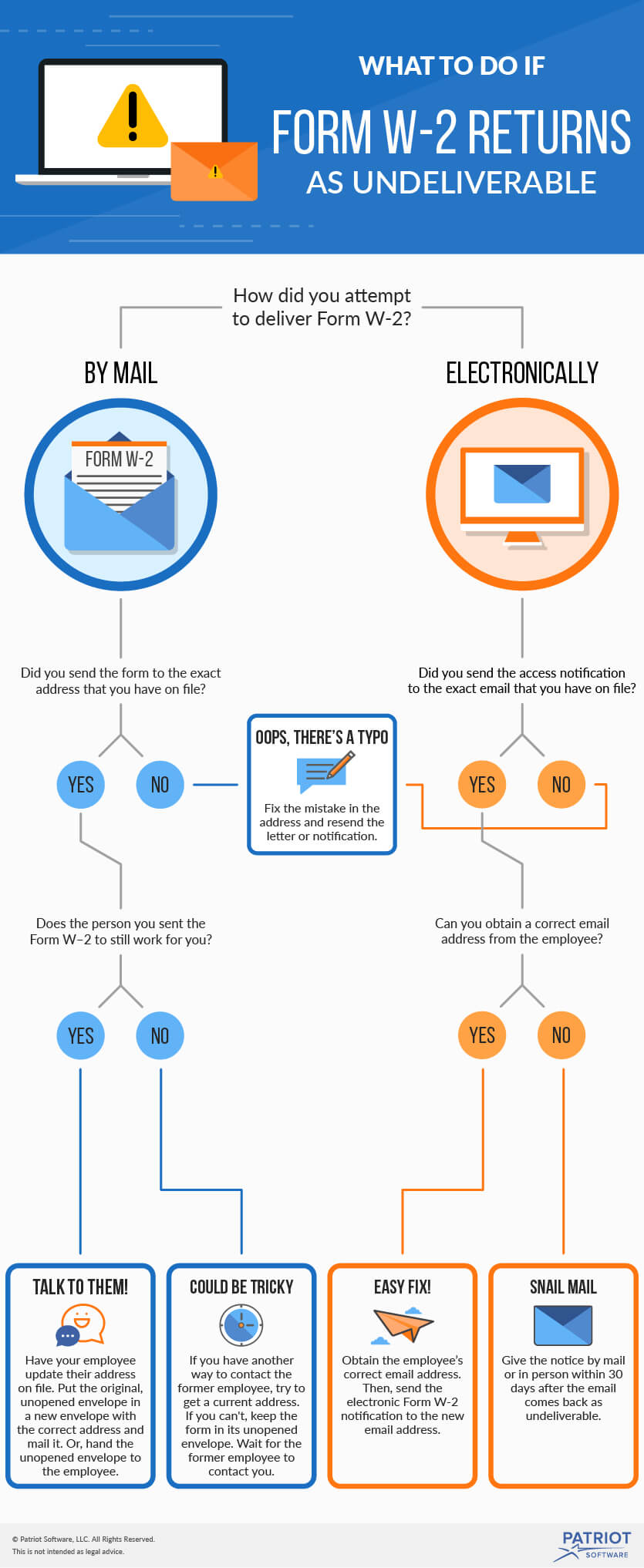

Form W-2 returned to employer

What you do with an undeliverable Form W-2 depends on how you originally sent the form: by mail or electronically. Also, what you do depends on if the worker is a current or former employee.

Paper Form W-2

You can mail paper copies of Form W-2 to employees. If one of the forms is returned to you as undeliverable, do not open the envelope. The sealed envelope with its postmark serves as proof that you attempted to send the Form W-2 on time.

Make a copy of the envelope and keep the copy in your records. The envelope copy allows you to retain proof that you tried to send the form on time.

Check the address on the envelope with the address in your records. Make sure they match. If there is a typo on the envelope, place the original, unopened envelope in a new envelope and mail it to the correct address.

If the address on the envelope and the employee records do match, what you do next depends on if the employee still works for you.

Current employee

If the employee still works for you, talk to him or her. Ask the employee to provide you with a current address. This is also a good opportunity for the employee to update payroll files and other personnel documents.

With a current employee, you might be able to hand the Form W-2 directly to them. If you need to re-mail the form, do not take the Form W-2 out of the original postmarked envelope. Keeping the form in the sealed, postmarked envelope shows proof that you tried to send the form on time.

Place the sealed form in a larger envelope and mail it. The postmarks on both envelopes leave a trail that proves your effort to get the form to the employee.

Former employee

You might have an employee who quit or was fired during the past year. If so, getting a Form W-2 to an employee could be tricky, especially if they moved.

If the address on the envelope and the address in your file do match, there is not much you can do. You might try to contact the former employee if you have their phone number or email address.

Keep the sealed and postmarked envelope as proof that you attempted to send the Form W-2. You’ll want to keep a copy of the former employee’s Form W-2 on record for four years. The copy can be either a paper or an electronic copy.

Do not send the undeliverable form to the Social Security Administration.

At this point, the former employee should contact you to get the form. Do not send the form based on a request over the phone. Phone requests are more likely to be scams than written requests are. If possible, have the former employee give you a signed, written request.

When a former employee requests their Form W-2, place the original envelope in a new envelope. Then mail the form to the address the former employee provided you with.

Electronic Form W-2

You can electronically give Form W-2 to employees. When you electronically provide Forms W-2, post the forms on a secure website, like your payroll provider’s employee portal software or your business’s intranet. Then, you must give employees a notice that the Forms W-2 are available. You can give the notice by email, by mail, or in person.

The email notice might come back as undeliverable if an employee’s email address is incorrect. You should first try to obtain a correct email address. If you cannot do that, you must give the notice by mail or in person within 30 days after the electronic notice comes back as undeliverable.

Share Our Infographic On Your Site

For more payroll training, visit Patriot Software today!

When you use Patriot’s Full Service Payroll software, we will handle payroll taxes and submit forms for you. After the end of the year, you can print Forms W-2 and mail them to your employees. Get a free trial today!

This article is updated from its previous publication date of 11/15/2014.