An estimated 3.4 million workers deal with independent contractor misclassification.

When you bring someone on board, determine whether the worker is an independent contractor or employee. It’s no secret that the IRS has strict policies in place to crack down on employers who misclassify contractors. So, how do you avoid misclassifying independent contractors?

Independent contractor vs. employee classification

Before we dive into more about workers misclassified as independent contractors, let’s briefly recap the difference between independent contractors and employees.

If your worker has employee status, you must withhold, match, and remit payroll taxes. Employers who classify a worker as an independent contractor are not typically responsible for withholding taxes.

Independent contractors

An independent contractor may run their own business. However, they also perform work for other companies.

You don’t deduct payroll taxes from independent contractors’ wages. They pay their own self-employment and income taxes. Instead of receiving Form W-2, contractors receive Form 1099-MISC to report wages.

In most cases, contractors take on multiple projects or jobs, provide their own tools, decide how jobs are done, work for multiple employers, and perform supplementary tasks.

Employees

Employers withhold Social Security, Medicare, and federal income taxes from employee wages. When you compensate an employee, you are also responsible for paying certain employer taxes and contributions.

Employees receive Form W-2, Wage and Tax Statement. An employee’s Form W-2 shows how much you paid them and withheld in taxes.

Typically, employees are eligible for overtime, receive supervision and instructions, don’t provide tools and resources, work for a single employer, and perform key business tasks.

Guidelines for classifying workers

As an employer, there are specific guidelines you must follow to assess a worker’s status. Both the Fair Labor Standards Act (FLSA) and IRS have classification regulations.

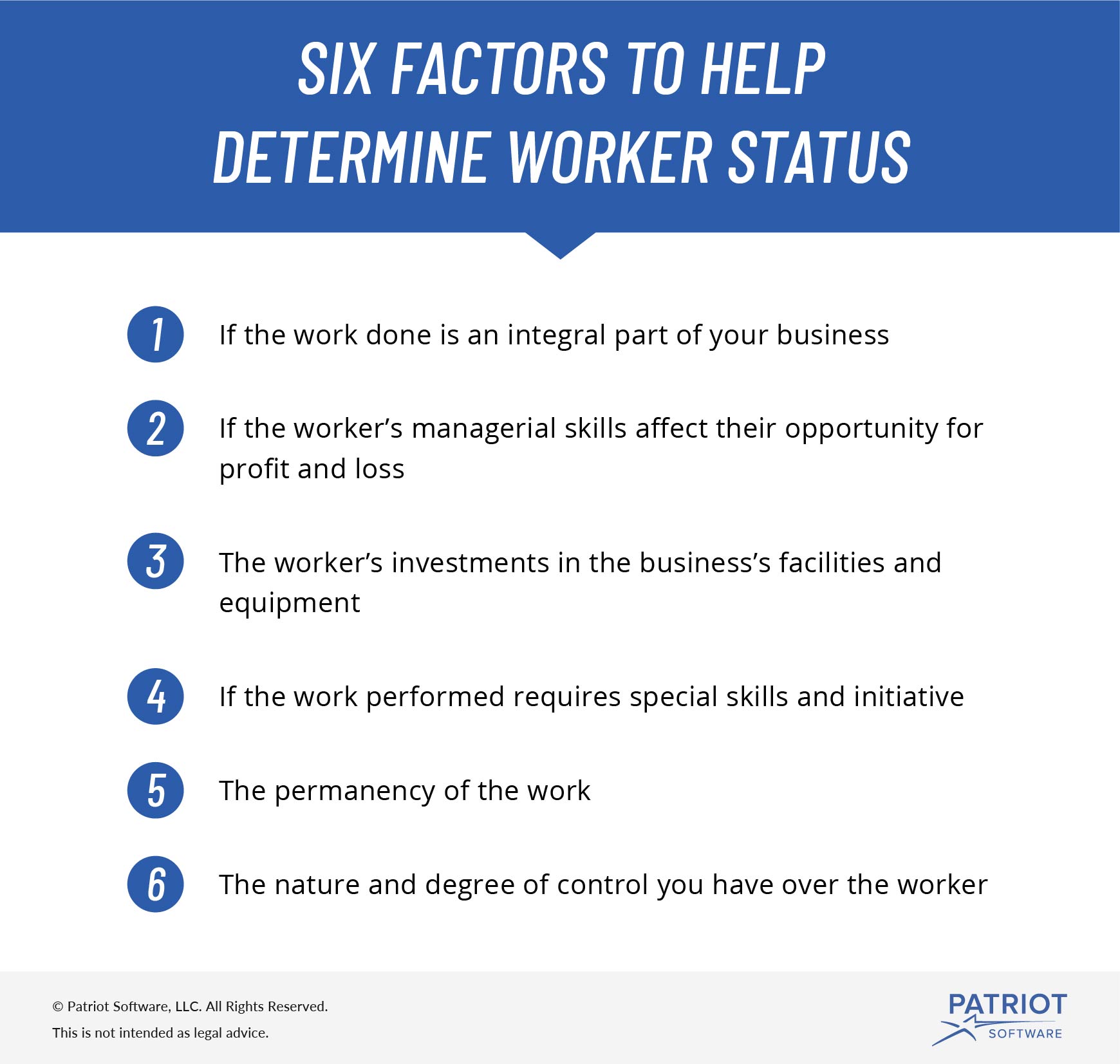

The FLSA provides six factors to help determine worker status. These include:

- If the work done is an integral part of your business

- If the worker’s managerial skills affect their opportunity for profit and loss

- The worker’s investments in the business’s facilities and equipment

- If the work performed requires special skills and initiative

- The permanency of the work

- The nature and degree of control you have over the worker

Keep in mind that you must consider all of the above points to help determine worker classification.

The IRS also has specific guidelines to help you figure out whether your worker is an employee or independent contractor.

Generally, a business that contracts a worker tells the contractor the scope of the work but doesn’t have control over how the contractor completes the assignment.

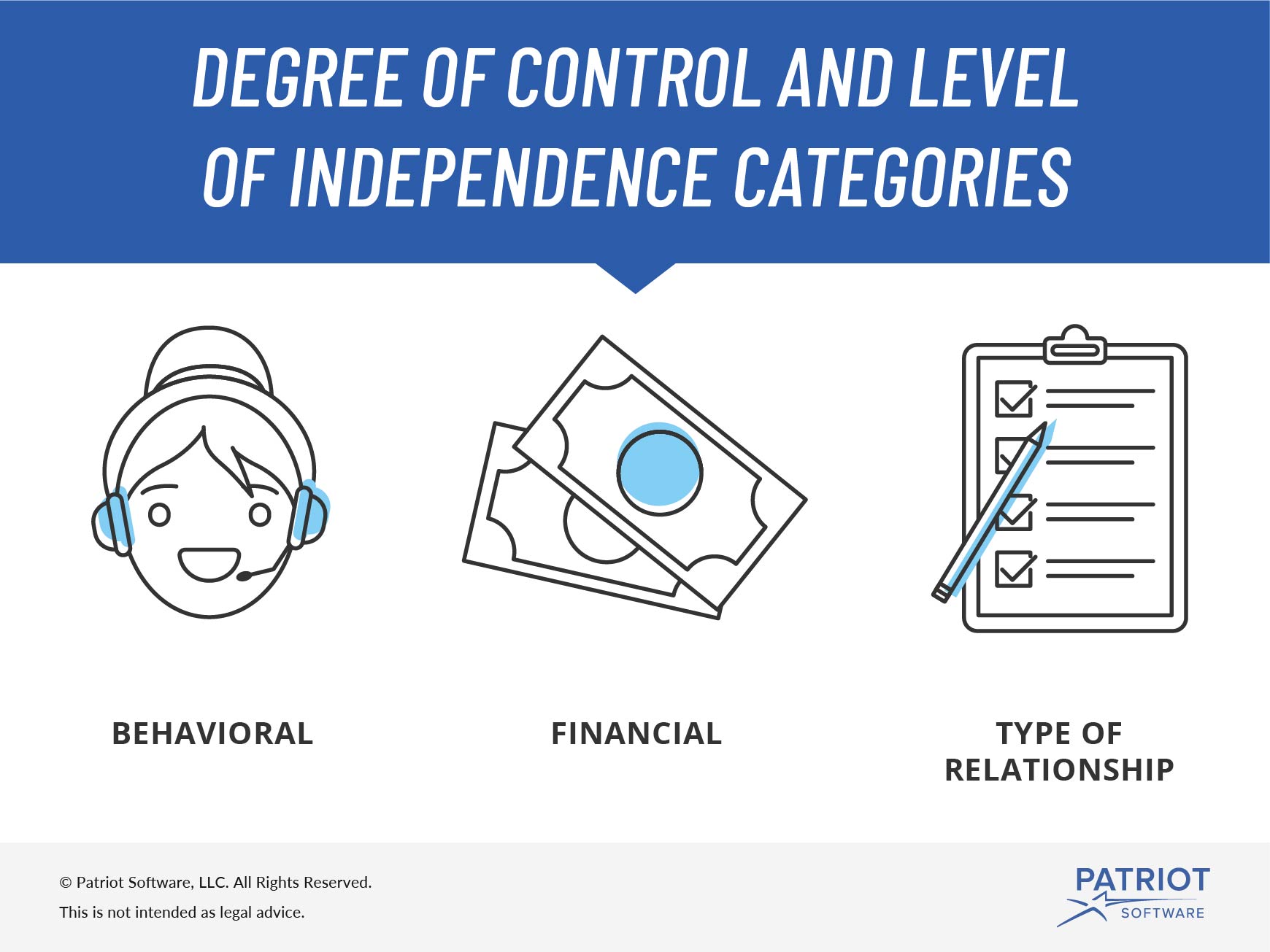

Based on these main factors, the IRS breaks down the degree of control and level of independence into three categories:

- Behavioral

- Financial

- Type of relationship

Before classifying a worker, consider how much control you have over them in the three areas above.

Behavioral

When looking at behavioral control, think about whether your company has the ability and right to control what the worker does and how they complete a project.

If you can control it, the worker may fall into employee territory. And if you can’t control what the worker does and how they do it, they are more likely an independent contractor.

Financial

For this category, ask yourself, Are you able to control other business aspects of the worker’s job? For example, things like how you pay the worker, how you handle expense reimbursements, and who provides supplies and tools can impact the status of a worker.

If you have control over the above examples (e.g., you provide the worker their supplies), you likely have an employee on your hands.

Type of relationship

Take a look at your employer-worker relationship. Are there any written contracts in place? Do you provide the worker with any types of benefits, such as health insurance? Will the relationship continue after the worker finishes their duties?

Asking yourself these types of questions can help you decipher if your worker is a contractor or employee.

For example, independent contractors likely have a written contract but do not receive benefits like employees.

Reasons why employers misclassify workers

Many small business owners do not purposefully misclassify their workers. Some lack the proper guidance and knowledge and misclassify a worker by accident. However, not all employers misclassify their workers unintentionally.

Employers might misclassify workers on purposes to avoid additional expenses such as:

- The employer portion of Social Security and Medicare taxes

- Overtime pay

- Employee benefits (e.g., paid time off)

- Unemployment tax

- Workers’ compensation insurance

Independent contractor misclassification penalties

The IRS and Department of Labor (DOL) are strict on employee misclassification. If you do misclassify a worker, the IRS and DOL can impose some hefty penalties, regardless of if it was intentional or not.

If the IRS and DOL deem the misclassification as unintentional, some penalties may include:

- Paying fees for not filing Forms W-2

- Owing money for taxes (e.g., employer contribution of FICA tax)

If the IRS and DOL suspect the misclassification was intentional, they may charge you the following penalties:

- Up to one year in prison

- Being labeled a “tax evader”

- Up to $500,000 in fines

How to protect yourself from worker misclassification

When you hire a worker, you may find it difficult to classify a worker on your own. If you have trouble with this determination, you can consult a small business lawyer, reach out to another professional, or file Form SS-8.

Form SS-8, Determination of Worker Status for Purposes of Federal Employment Taxes and Income Tax Withholding, determines the status of a worker (e.g., independent contractor vs. employee).

You or your worker can file Form SS-8 if you’re unsure of a worker’s classification.

File Form SS-8 by mailing the form to the IRS. You cannot electronically file Form SS-8 or send it to the IRS via fax. There is no fee to file Form SS-8.

After you file Form SS-8, the IRS sends one of three letters to you and your worker:

- Determination letter: Binding notice that urges the business to change the worker’s classification

- Information or courtesy letter: Notice that could help your worker complete federal tax obligations (not binding)

If you have any additional questions about Form SS-8 requirements and process, contact the IRS.

What to do if you misclassify a worker

If you classified a worker as an independent contractor and the IRS determines they are an employee, immediately change the worker’s status from contractor to employee. Add your newly classified employees to your payroll, withhold payroll taxes, and begin offering benefits to employees.

Misclassified workers might also need to file Form 8919, Uncollected Social Security and Medicare Tax on Wages.

Need help keeping track of independent contractors? Patriot’s online accounting software lets you record vendor payments, create invoices, and much more. And, we offer free, U.S.-based support. What are you waiting for? Start your self-guided demo today!

We’re always ready to keep the conversation going. Give us a like on Facebook and share your thoughts on our latest articles.

This article has been updated from its original publication date of October 4, 2012.

This is not intended as legal advice; for more information, please click here.