In business, it seems like you dole out money for anything and everything. Employee wages and inventory purchases are just some of the payments you might make. Sometimes, you may make payments that fall under the IRS’s miscellaneous category. And if you do, you must report them as miscellaneous information (formerly miscellaneous income).

So, what is miscellaneous information, how does it differ from nonemployee compensation, and how do you report it?

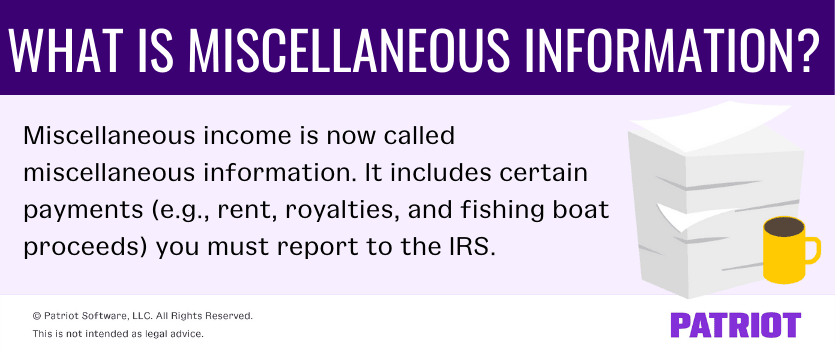

What is miscellaneous income (information)?

If you make certain IRS payments to 1099 vendors, you must report the money as miscellaneous information on Form 1099-MISC, Miscellaneous Information. Previously, these types of payments were called miscellaneous income.

The IRS considers a few payments as miscellaneous. So, what kind of miscellaneous income do you need to know about?

Miscellaneous income includes:

- Rent payments

- Royalties

- Fishing boat proceeds

- Medical and health care payments

- Crop insurance proceeds

- Fish purchases paid in cash for resale

- Gross proceeds to an attorney

- Other income payments (e.g., prizes and awards)

Businesses must report qualifying miscellaneous income on Form 1099-MISC to the IRS for tax purposes. You must also report direct sales totaling $5,000 or more and excess golden parachute payments on the form.

Keep in mind that Form 1099-MISC is just one type of information return you may use to report payments.

Prior to 2020, miscellaneous income also included “nonemployee compensation,” which is the amount you pay independent contractors. Nonemployee compensation is now separate from miscellaneous information. Instead of reporting independent contractor payments on Form 1099-MISC, report them on Form 1099-NEC, Nonemployee Compensation.

How to report miscellaneous information

As a business owner, you must report miscellaneous payments you make on the 1099-MISC tax form. Individuals receiving Form 1099-MISC use the information to report their miscellaneous earnings on their federal tax returns.

Include the amount you paid for each type of miscellaneous information that exceeds $600. If you paid royalties, report amounts over $10.

Report miscellaneous information in the appropriate boxes:

| Box | Category | Details |

|---|---|---|

| Box 1 | Rents | If you rent a physical location for your business and don’t pay a real estate agent or property manager, the payments are considered miscellaneous. Also include machine and pasture rentals as miscellaneous information. |

| Box 2 | Royalties | Payments made to someone for the use of property (e.g., patents, copyrights, etc.), are considered miscellaneous information. |

| Box 3 | Other income | This type of miscellaneous information includes any other type of 1099-MISC payment that doesn’t fall under a specific category. Examples include prizes and awards and a deceased employee’s wages paid to a beneficiary. |

| Box 3 | Prizes and awards | Report any money you paid in prizes and awards that are not for services performed (e.g., amounts paid to a sweepstakes winner not involving a wager). |

| Box 3 | Notional principal contract | If you paid any cash from a notional principal contract to an individual, partnership, or estate, report the amount here. |

| Box 5 | Fishing boat proceeds | Report each crew member’s share of all proceeds from the sale of a catch or the fair market value of a distribution if the fishing boat has normally fewer than 10 crew members. |

| Box 6 | Medical and health care payments | If you made payments in the course of your trade or business to physicians or other medical and health care suppliers or providers, report the amount here. |

| Box 9 | Crop insurance proceeds | Insurance companies report crop insurance proceeds paid to qualifying farmers. |

| Box 10 | Gross proceeds paid to an attorney | Payments made to an attorney in connection with legal services, but not for the attorney’s services, are miscellaneous income. |

| Box 12 | Section 409A deferrals | If you opt to complete Box 12, report deferred amounts for nonemployees under nonqualified plans. Keep in mind that completing this box isn’t mandatory. |

| Box 14 | Nonqualified deferred compensation | If you deferred amounts includible in income under a section 409A because the nonqualified deferred compensation plan doesn’t meet the requirements, report it here. |

Of course, you also need to enter information like the name, address, and identification number of the person you made the payment to on Form 1099-MISC. And, include your business information.

There are also additional boxes on Form 1099-MISC you can use to report extra information, like taxes withheld and excess golden parachute payments.

What to do next

After reporting miscellaneous payment amounts in the appropriate boxes on Forms 1099-MISC, distribute them to the appropriate parties:

- Copy A: IRS

- Copy 1: State tax department (if applicable)

- Copy B: Recipient

- Copy 2: Recipient (to be filed with their state income tax return)

- Copy C: Your records

You can mail or e-File Forms 1099-MISC with the IRS.

Submit Forms 1099-MISC to the recipient by January 31 of each year. File the forms with the IRS by February 28 (paper) or March 31 (filing electronically).

For more information on miscellaneous information, consult the IRS’s website.

This article has been updated from its original publication date of July 17, 2013.

This is not intended as legal advice; for more information, please click here.