When you have a business, you have direct and indirect costs. Tracking these expenses is key to having up-to-date books, receiving tax deductions, and making business decisions. So, what’s the difference between direct vs. indirect costs?

Direct vs. indirect costs

Lumping your expenses together is a recipe for inaccurate recordkeeping, reporting, and decision-making. Understand the difference between direct and indirect expenses to avoid these issues.

Direct cost definition:

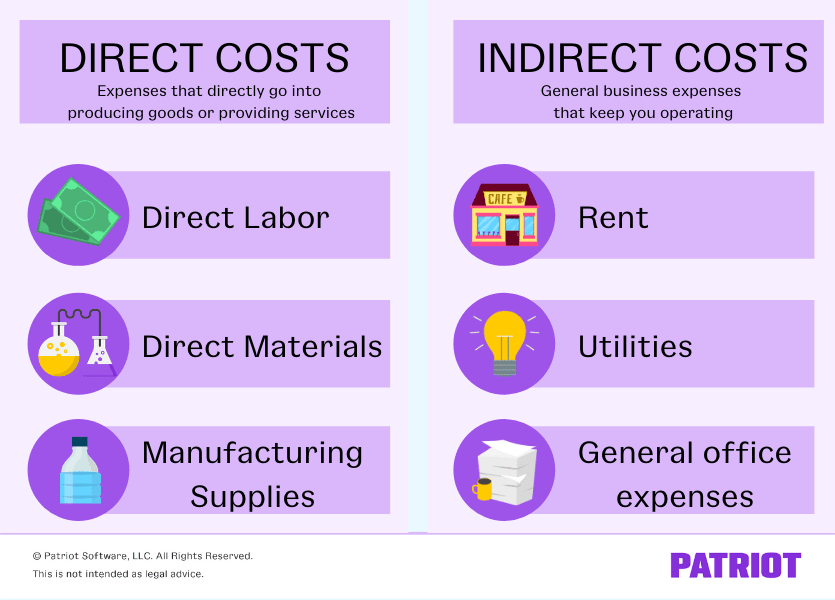

Direct costs are business expenses you can directly apply to producing a specific cost object, like a good or service. Cost objects are items that expenses are assigned to.

Examples of direct costs include:

- Direct labor

- Direct materials

- Manufacturing supplies

Direct costs can be variable or fixed. Variable costs are expenses that change based on how many items you produce or how many services you offer. For example, you would spend more money producing 200 toys as opposed to 100 toys. Fixed costs are expenses that remain the same each month.

Knowing your direct costs is a key part of determining your product or service pricing. You want to make sure customers pay you more than what you pay to produce your products or offer your services.

Example

Let’s say you have an employee who puts together toys. The employee’s work is considered direct labor. To create the toys, the employee needs wood, which is considered a direct material. And, the employee must use wood glue, which is a manufacturing supply.

Knowing the costs that go into producing the toys helps you better price the goods and turn a profit.

Indirect costs definition:

Indirect costs are expenses that apply to more than one business activity. Unlike direct costs, you cannot assign indirect expenses to specific cost objects.

Examples of indirect costs include:

- Rent

- Utilities

- General office expenses

- Employee salaries (e.g., administrative)

- Professional expenses

- Other overhead costs

Like direct costs, indirect expenses can be either fixed (e.g., rent) or variable (e.g., utilities).

You can allocate indirect costs to determine how much you are spending on expenses compared to your sales. To do this, find the overhead rate, or indirect cost ratio.

Here is the overhead rate formula:

Overhead Rate = Overhead Costs / Sales

Example

Let’s say you make rent and utility payments to keep your business going. And, you must buy computers. These costs are not directly related to producing a specific product or performing a service, so they are indirect costs. Indirectly, they help you produce goods and perform services, but you can’t directly apply them to a specific product or service.

To get an idea of how your overall expenses compare to your overall sales during a period, you find your overhead rate.

You had $4,000 in indirect costs and $16,000 in sales during the period. Your overhead rate would be 0.25, or 25% ($4,000 / $16,000). This means that you spend 25 cents on indirect costs for every dollar you earn. If your direct costs are also high, you won’t be turning much of a profit.

Overhead rates vary from industry to industry. But, you should try to keep your overhead rate minimal. The smaller your overhead rate, the better.

Why does the difference between direct and indirect cost matter?

To sum up, direct costs are expenses that directly go into producing goods or providing services, while indirect costs are general business expenses that keep you operating. But, why does the difference matter?

Direct vs. indirect expenses for income statements

Knowing which costs are direct vs. indirect helps you with recording expenses in your books and on your business income statement.

Your income statements break down your business’s profits and losses during a period. When creating your income statement, you have different line items for income and expenses like revenue, cost of goods sold (COGS), and operating expenses.

You wouldn’t record an indirect cost under COGS on the income statement. Instead, you should list indirect costs under business expenses.

Direct cost vs. indirect cost for taxes

When it comes to claiming tax deductions, you need to know the difference between direct vs. indirect costs.

Why? Because the IRS says so. According to the IRS, you must separate your business expenses from the expenses you use to determine your cost of goods sold (e.g., direct labor costs).

You must subtract your COGS from your business’s gross receipts to figure out your gross profit on your business tax return. When you classify an expense in your COGS, you can’t deduct it as a business expense.

Business expenses like rent and employee wages are just some of the deductions you can claim. But to do so, you need to have accurate and detailed records to back up your claims.

Misclassifying your direct and indirect expenses when claiming deductions could cause you to come under IRS scrutiny. Not to mention, failing to break down your costs could cause you to miss out on a tax deduction.

Pricing products with direct cost vs. indirect cost

To run your business, you must take all expenses into account. Doing so is key to budgeting. But, what about pricing products? How can you apply your direct and direct costs to an individual product or service?

Sure, you can look at your cost of goods sold to see how much it costs to produce a good. However, COGS only show you direct costs, not indirect ones.

To find out how much it truly costs you to produce a product or perform a service, you might also consider an activity-based costing (ABC) system.

With the ABC system, you can allocate your overhead costs to certain activities, and thus products, to get a more specific picture of your cost by product.

This article has been updated from its original publication date of March 22, 2018.

This is not intended as legal advice; for more information, please click here.