When you run a small business, one error in your accounting books can result in inaccurate financial statements, poor cash flow management, and even an IRS audit. To make sure your records are accurate, familiarize yourself with account reconciliation.

What is account reconciliation?

Account reconciliation is the process of comparing the numbers in an account with another financial record to verify the balances match. By reconciling the accounts, you can catch errors in your journal entries and general ledger for small business. If the records don’t match, you must modify the account balance.

You might compare an account to your bank statements, credit card statements, receipts, or related records. You can reconcile your accounts daily, monthly, semiannually, or annually.

For example, you can compare a cash account to your business bank statement. When you receive your bank statement, verify that its bottom line matches the bottom line in your account.

Think of account reconciliation like proofreading for accounting. If you don’t reconcile accounts, your information may be incorrect, unclear, or misleading. But when you take the time to spot errors early on, you can avoid significant issues down the road.

Purpose of account reconciliation

Reconciling accounts is a smart decision for all small businesses. Not to mention, some companies are required to regularly reconcile accounts to comply with generally accepted accounting principles (GAAP).

Again, the purpose of account reconciliation is to verify that your account information is accurate and consistent. Maintaining up-to-date records prevents a number of business setbacks.

Reconciling your accounts can help you:

- Prevent overspending

- Stop fraudulent activity

- Create accurate financial statements

If you don’t reconcile your accounts, you could overdraft an account. You may think you have more money in the account than you have if your numbers are incorrect.

For example, your cash account shows a balance of $1,000, so you decide to buy a $780 computer. However, you first reconcile your cash account and discover that the actual balance is $600. Because you reconciled your account, you don’t overdraft your account.

Failing to reconcile your accounts can also lead to unnoticed fraudulent activity. An employee might create inaccurate journal entries to pay themselves more money.

Let’s say an employee commits payroll fraud and pays themselves more than they earned. You reconcile your payroll journal entries with your payroll account and notice that more money is leaving your payroll bank account than what you recorded in your books. As a result, you can terminate the thieving employee and avoid further fraudulent activity.

When your accounts have incorrect information, you will create inaccurate financial statements. Financial statements show you information about your business’s financial health, including your profits and losses, assets and liabilities, and cash flow. You must create accurate financial statements to make business decisions and secure financing from investors or lenders.

Account reconciliation process

Are you ready to reconcile your accounts? Use the following reconciliation process steps for consistent records.

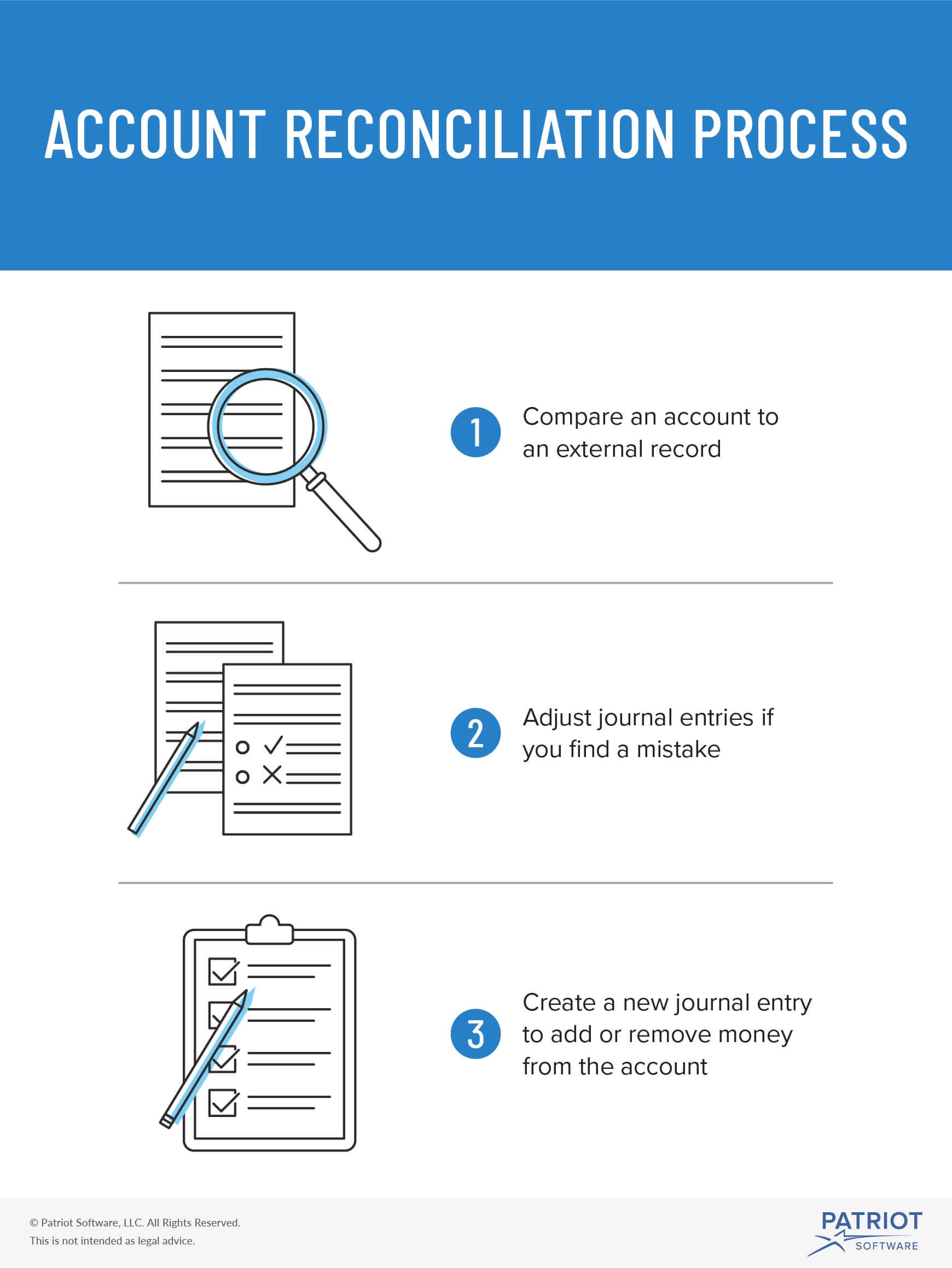

First, compare an account to the appropriate external record. If you find a mistake in your account, adjust your journal entries. You can create a new journal entry to add or remove money from the account.

When you reconcile your accounts, be sure to keep all supporting documents in your records. By storing documents, you can back up why you made changes to your account balances.

Looking for an easy way to track and reconcile your accounts? Patriot’s online accounting software makes it easy to record income and expenses. Plus, we offer free, U.S.-based support. Get your free trial today!

This is not intended as legal advice; for more information, please click here.