Like any business, you need up-to-date accounting records if you run a farm, ranch, or related operation. But, some aspects of agricultural accounting—like livestock and land—are specific to farming businesses.

Read on to learn:

- What’s considered a “farm business?”

- Agricultural accounting Q&A

- Farm accounting tax forms

What’s considered a “farm business?”

Unsure if your operation qualifies as a farm business? According to the IRS, you have a farm business if you “cultivate, operate, or manage a farm for profit, either as owner or tenant.”

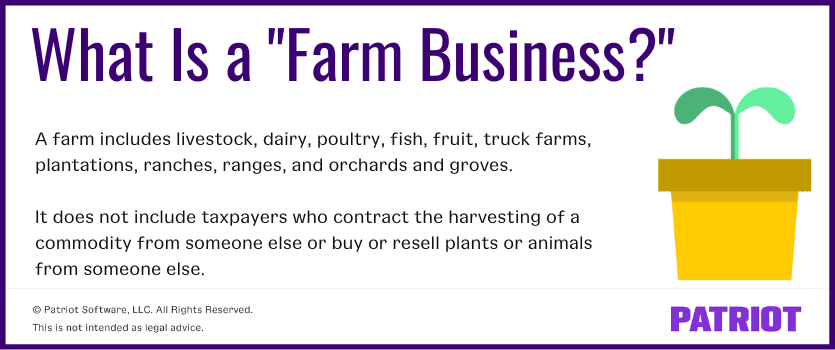

A farm includes:

- Livestock

- Dairy

- Poultry

- Fish

- Fruit

- Truck farms

- Plantations

- Ranches

- Ranges

- Orchards and groves

You do not have a farming business if you 1) contract the harvesting of a commodity from someone else or 2) buy or resell plants or animals from someone else.

Agricultural accounting Q&A

Agricultural accounting, or AG accounting, is the process of accounting for your farm, ranch, or related business. Keeping accurate and up-to-date records helps you to prepare for tax time, create financial statements, make informed decisions, and measure your farm’s financial health.

Sure, you must record the transactions that take place like in regular business accounting. But as an AG business, you also need to record your stock levels and the market value of your land.

Having up-to-date records also helps you better plan for, take advantage of, and record government subsidies for farmers.

So without further ado, here are some answers to common questions farming businesses may have.

1. What are the methods of accounting for agriculture business?

Farm businesses must choose an accounting method for recording income and expenses. Generally, a business can choose between cash-basis, accrual, and hybrid accounting methods.

For agricultural accounting, most farmers use the cash method. Cash-basis accounting is the easiest of the three accounting methods in terms of recordkeeping. Under the cash method, record your gross income in the tax year you receive it. And, you typically deduct expenses in the tax year you paid for them.

However, not all farm businesses can use the cash method. You must use the accrual method if your farm business is a:

- Corporation with gross receipts of more than $26 million

- Partnership that’s partnered with a corporation that has gross receipts of more than $26 million

- Tax shelter

Under accrual accounting, you generally report income in the year earned and deduct or capitalize expenses in the year incurred. You must also use the accrual method to determine your farm’s gross income if you keep an inventory.

2. What is considered farm income?

You must know what farm income is for recordkeeping purposes. That way, you can accurately report your business income when you file your annual small business tax return.

Farm income includes income from:

- Operating a stock, dairy, poultry, fish, fruit, or truck farm

- Operating a plantation, ranch, range, orchard, or grove

- The sale of crop shares if you materially participate in producing the crop

- Operating a nursery that specializes in growing ornamental plants

- Government payments/subsidies (e.g., payments for approved conservation practices, livestock forage disaster, etc.)

- Crop insurance payouts you receive due to crop damage, reduction of crop revenue, or both

- Feed assistance and other benefits from the Secretary of Agriculture

3. What are farm business expenses?

Reporting income in your accounting books is just part of the fun—you need to report expenses, too. And in farm accounting, there are deductible and nondeductible expenses.

Deductible farm expenses are ordinary (what farmers do) and necessary (what’s useful and helpful in farming) costs. These include qualifying:

- Prepaid farm supplies

- Prepaid livestock feed

- Wages paid for regular farm labor, piecework, contract labor, and similar forms of labor

- Repairs and maintenance of farm property (e.g., repainting, maintenance on trucks or tractors, etc.)

- Farming business interest paid or accrued

- Breeding fees

- Fertilizer, lime, and other materials you apply to farmland to enrich, neutralize, or condition it (if those benefits last a year or less)

- Real estate and personal property taxes on farm business assets (e.g., farm equipment, animals, etc.)

- Insurance for your farm (e.g., crop, fire, storm, theft, or liability insurances)

- Property you lease for use in your farm

- Accounting fees

- Advertising expenses

- Farm-related attorney fees

- Recordkeeping expenses

- Utilities and internet

Nondeductible farm expenses include personal, living, and family expenses, such as the cost of maintaining your personal vehicles or horses. You also cannot deduct expenses such as loan repayment, loss of livestock (if you deducted the cost of raising them as an expense), or membership fees (e.g., country club).

4. How do I account for the weather?

Droughts. Floods. Tornadoes. Hurricanes. When you run a farm, so much is outside of your control.

Document the weather if it causes you to see or exchange more livestock than you normally would. The IRS lets certain farm businesses postpone reporting the gain from additional animal sales if you can prove that the sale was weather-related.

Determine how much livestock you would have sold without the weather-related condition. And when you postpone the gain, be ready to back up your math. Pull your AG accounting records from past years to show how many animals you’ve sold, how many animals you would have sold without the weather-related conditions, and other proof.

5. How does depreciation work?

You probably have several pieces of equipment you use for your farm, including:

- Machinery

- Equipment

- Buildings

- Vehicles

- Furniture

- Livestock

- Copyrights and patents

Overtime, assets depreciate, or lose value. You can depreciate property you own and use on your farm if it has a determinable useful life that is longer than the year you begin using it. Determine your annual depreciation across your farm assets to claim a tax deduction.

Heads up! Don’t try to depreciate your land. Unlike machinery and other types of property, land does not wear out. Instead, it likely increases in value.

6. What kind of records do I need to keep?

You must keep all records that show your farming business’s income and expenses. This includes supporting documents for purchases, sales, payroll, and all other business transactions.

Take a look at the following examples of records you need to keep for agricultural accounting:

- Invoices

- Receipts

- Business bank statements

- Canceled checks

Inventory records

Do you keep an inventory? If so, you need to record all aspects of your inventory in your farm records, including:

- Eggs in the process of incubation

- Harvested and purchased farm products held for sale or feed or seed (e.g., grain)

- Livestock held primarily for sale

- Crops with a reproductive period of more than two years, if applicable

7. How long do I need to keep records?

According to the IRS, the length of time you need to keep records relating to your farming business depends on the record type.

Business tax return records: Generally, you need to keep records that support an item of income or a deduction on your business tax return for at least three years from when your tax return was due or filed or within two years of the date the tax was paid (whichever is later).

Employment tax records: If your farm business employs employees, keep employment tax records for at least four years after the date the tax becomes due or is paid (whichever is later).

Asset records: Retain property-related records until the period of limitations expires for the year you dispose of the property. That way, you can figure out any depreciation, amortization, or depletion deduction. You can also determine your gain or loss.

8. Is there anything else I should know?

Yes! Accounting for farming operations can be tricky. There are a lot of special rules you may need to know.

To help you stay on top of your agricultural accounting responsibilities, you may consider using accounting software to handle your day-to-day recordkeeping and hiring an accountant.

For more information on the ins and outs of farm business accounting, consult IRS Publication 225, Farmer’s Tax Guide.

Farm accounting tax forms

As a farm business owner, you must use certain tax forms specifically for agricultural operations. Three common farm tax forms include:

- Schedule F

- Schedule J

- Form 943

Schedule F

Schedule F (Form 1040), Profit or Loss from Farming, is a tax form to report farm income and expenses.

Attach Schedule F to your tax return if you are an individual, trust, partnership, S Corp, or LLC with a farm business. Corporations use Form 1120, U.S. Corporation Income Tax Return.

Report your income and expenses on Schedule F based on your agricultural accounting method.

Schedule J

Schedule J (Form 1040), Income Averaging for Farmers and Fishermen, is a form you can use to average your taxable farm income.

You can use Schedule J to average your taxable income over the previous three years. That way, you can potentially lower your tax liability if your income is high one year and low in another.

Form 943

Non-farm businesses typically report employment wage and tax information on Form 941, Employer’s Quarterly Federal Tax Return, or Form 944, Employer’s Annual Federal Tax Return.

Similarly, Form 943, Employer’s Annual Federal Tax Return for Agricultural Employees, is an employment form employers use to report wage and tax information.

You must file Form 943 if you paid wages subject to employment tax (federal income, Social Security, and Medicare) withholding to one or more farmworkers.

Wages are subject to employment tax withholding if one of the following is true:

- You pay cash wages of $150 or more to an employee during the tax year for farm work

- The total wages (cash and noncash) you pay all farm workers during the year is $2,500 or more

Quick must-knows of farm accounting

There’s a lot that goes into agricultural accounting. To help you make heads or tails of your responsibilities, here are some quick reminders:

- You have a farm business if you cultivate, operate, or manage a farm for profit

- Most farm businesses use cash-basis accounting, but some use accrual

- Do not depreciate land

- Report income and expenses on Schedule F

- Keep detailed tax return-related records for at least three years

- Consult IRS Publication 225 for more information

Looking for a better way to manage your accounting books? Patriot’s online accounting software makes it easy to track your income, record payments, and so much more. Try it for free today!

This is not intended as legal advice; for more information, please click here.